Behind India’s poor property tax collection

Explained mostly by just two institutional factors.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

What’s behind India’s poor property tax collection?

The world runs on a metal it can’t mine

What’s behind India’s poor property tax collection?

India’s property market has been booming for two decades. In our metropolitan and tier-1 cities, new construction seems to be everywhere, and real estate values have blown up manifold.

And yet, the tax most directly tied to all of this — the property tax — has been stuck at 0.15% of GDP for a long time. That’s half the rate of low-income countries, and a quarter of middle-income ones.

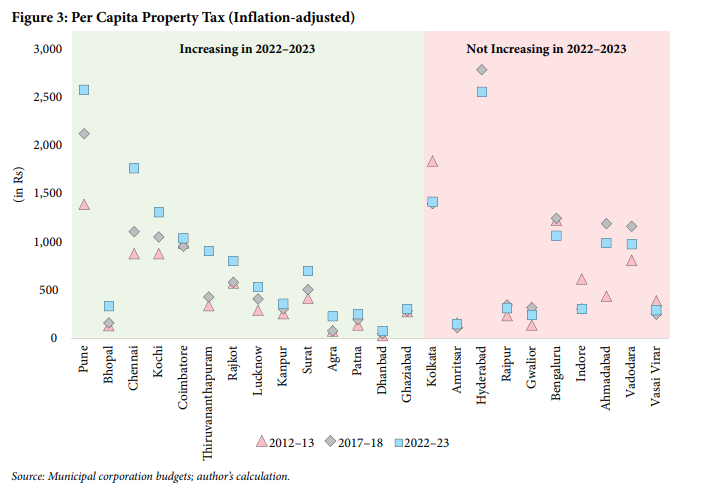

In 10 of India’s 24 largest cities, real per capita property tax actually declined over the last decade. The money is sitting right there, embedded in rising land values and new buildings, but cities aren’t collecting it.

A new working paper by Debarpita Roy of the Centre for Social and Economic Progress seeks to explain why it is so. It turns out that the answers largely boil down to two key institutional factors that govern property tax collection.

Whither decentralization?

In each Indian city, on paper, the power of collecting property taxes rests with the municipal corporation.

Formally introduced in 1992, municipal corporations were meant to create a genuine third tier of government that would relieve the state governments of some duties, and allow cities to govern themselves with elected councils and defined functions. Crucially, this would also mean that municipal corporations would have their own sources of revenue.

But what happened in practice reflects the complications of how power works in India’s government structure. And this is the first factor affecting India’s property tax governance.

After all, state governments retained control over staffing decisions, valuation frameworks, and the ability to delay or dissolve elected local bodies. Municipal corporations were held responsible for roads, water, drainage, and sanitation, but they had little control over the funding required to fulfill those duties. They still depend heavily on state transfers and grants.

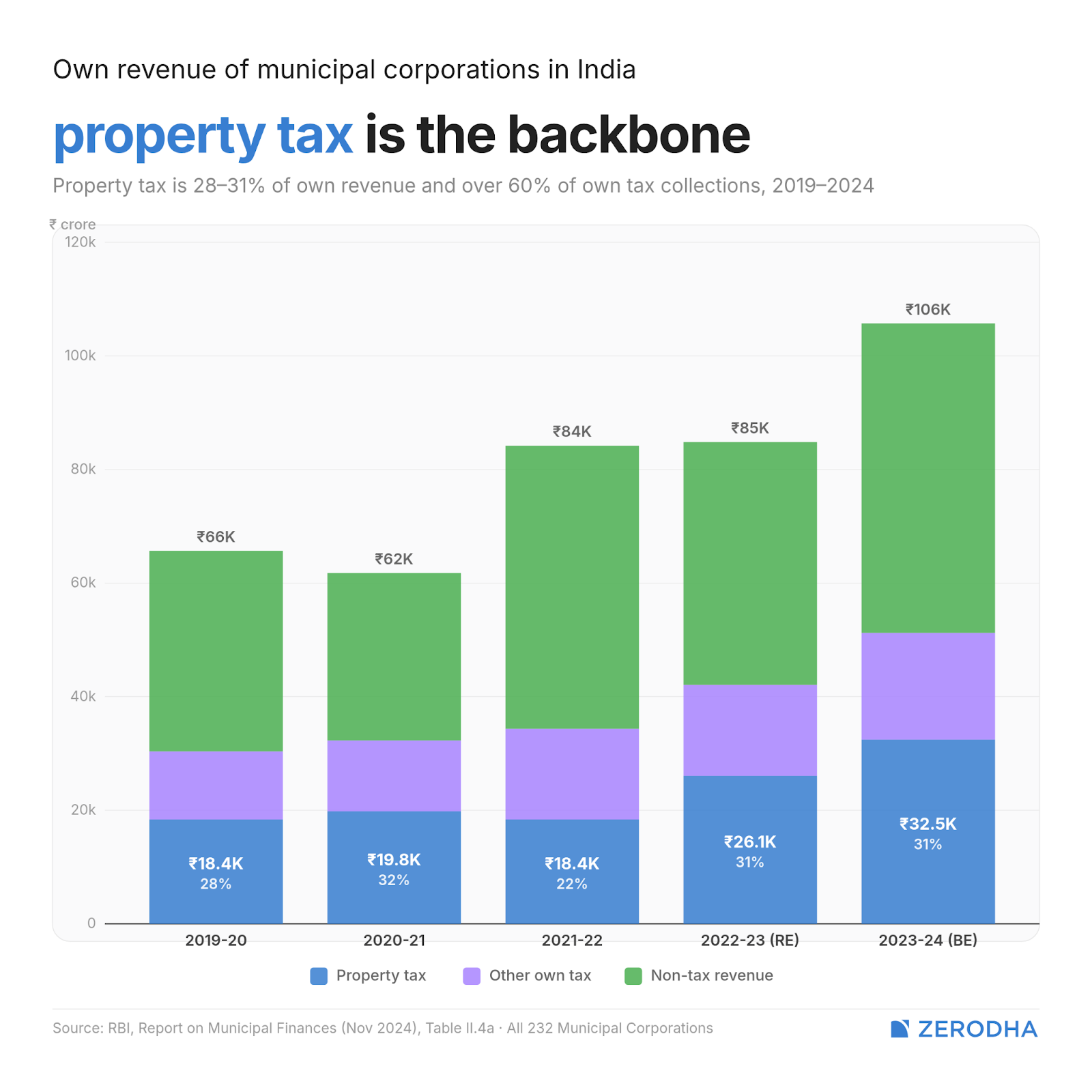

The property tax, though, was supposed to be different. It’s the one major revenue source that belongs entirely to the Urban Local Body (ULB). Over the years, it has often made up around 30% of own-source revenue (tax and non-tax) across all ULBs in India. With other local taxes absorbed into GST over the years, property tax has only become more central.

And yet, even this one tax that’s genuinely theirs is hemmed in at every stage by state-level decisions.

The paper outlines three stages of property tax collection. At first, you identify and keep a record of the properties. Secondly, you value the property and calculate the tax. Lastly, you bill the property owner and come to collect what’s due. Across each stage, though, the ULB is at a loss.

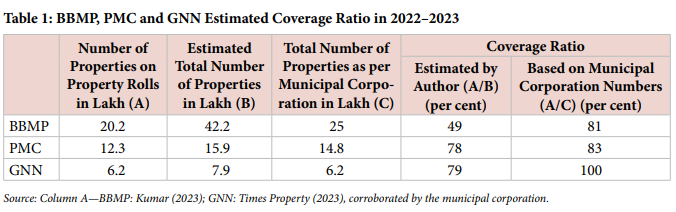

In the first stage itself, maintaining extensive coverage is very difficult for ULBs that are underfunded — and therefore, often understaffed. The paper estimates that Bruhat Bengaluru Mahanagara Palike (BBMP) — Bengaluru’s primary ULB — may have only 20 lakh properties on its tax rolls against an estimated 42 lakh total — a coverage ratio as low as 49%. Pune, meanwhile, is much higher at 78-83%.

Sometimes, technology might help in sidestepping this problem. For instance, GIS mapping drove Pune’s property roll growth from 2% per year to 7% per year in 2016-17. But GIS surveys need to be repeated, and BBMP’s last remote-sensing survey was over a decade ago.

More importantly, technology-based mapping still needs to be validated by physical inspections, door-to-door, by municipal staff. And municipal corporations chronically don’t have enough employees. The Karnataka Administrative Reforms Commission recommended a whopping 40% increase in BBMP’s property tax department headcount.

The poor capacity of ULBs affects the last stage of collection, too. Nominal collections have grown everywhere. But collection efficiency — what share of actual tax demand gets collected — has declined, and the ULB has plenty of backlog left. Pune’s outstanding arrears, for instance, have crossed ₹9,000 crore. Ghaziabad’s collection efficiency of total demand fell from 60% to 50% between 2015-16 and 2022-23.

Method to the madness

The second stage of estimating the property’s valuation, though, is the second major factor affecting India’s poor tax collection.

See, most Indian cities use what’s called an area-based valuation method. The municipal corporation sets a “base rate“ — expressed in rupees per square foot per month — and applies it to a formula that accounts for the property’s size, use, type of construction, and location zone. The result is the annual tax owed.

However, what this also means is that this base rate doesn’t move automatically when property values rise. It sits exactly where it was last set — until someone in the municipal corporation decides to revise it.

In other words, the base rate is not linked to the market.

The paper does outline a theoretically better alternative, called the capital value method. It would tie property tax to stamp duty guidance values, which are updated regularly by state governments. When property values rise, the tax base rises with them, automatically, without anyone having to make a decision.

But, this alternative is extremely political for one simple reason: property owners don’t want it.

Now, Bengaluru tried to switch. BBMP — the city’s municipal corporation — drew up draft capital value guidelines, capped the maximum increase, and put the proposal out. However, it was met by huge protests from citizens who would effectively see higher tax bills. What’s more, the state government also declined to support it. As a result, Bengaluru remained stuck on the area-based method.

Deadly cocktail

Put together, these two failures compound each other to make the failures bigger.

See, the area-based valuation design demands regular intervention in the base rate. But the institutional design makes that intervention nearly impossible. And sometimes, in response to that, the municipal corporation may adapt to their circumstances by adopting policies that make things even more difficult for them.

The dilemma presents itself in two ways.

Missing leaders

Consider what a base rate revision actually requires. For one, there needs to be a legal provision for it. Additionally, there needs to be citizen receptivity — people are more accepting of small, frequent increases than large one-time jumps. And lastly, there needs to be an elected municipal council in office.

That last condition often makes all the difference — for better and worse.

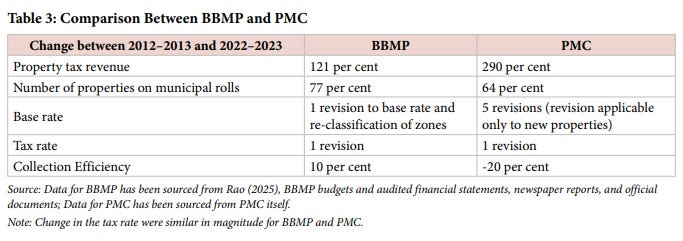

Pune, for instance, revised its base rate five times between 2012-2022. Over that period, property tax collections grew 290%. In contrast, over the same period, Bengaluru’s property tax collections grew 121%. This is despite the fact that Bengaluru added more properties to its rolls and actually improved collection efficiency more than Pune did.

Much of the contrast is explained by the base rate revisions Pune made and Bengaluru couldn’t. And in turn, the lack of base rate revisions was explained by the inconsistency in holding elections. After all, in that period, Pune enjoyed a functioning elected government. However, Bengaluru’s last municipal election was in 2015, while its last base rate revision was in 2017. Elections were due in 2020, but they still haven’t happened.

Since 2022, Maharashtra’s municipal elections — including Pune — have been on hold, and so have their base rate revisions. And several of India’s largest cities are currently being administered by state-appointed bureaucrats rather than elected councils.

Show me the money

The second example is an accounting problem that’s very common among municipal corporations.

In an ideal scenario, taxes would get recorded on the books of ULBs regardless of whether they were paid in cash immediately or not. This is called accrual-based accounting — what isn’t paid shows up as arrears. And, of course, this helps one calculate collection efficiency accurately.

However, ULBs barely have the capacity to follow-up on unpaid dues — which would be far higher if the base rate were actually revised. That’s why many ULBs follow cash-based accounting, where you only record what you received. More than half of India’s municipal corporations follow the cash-based method.

For those ULBs that do want to reform and ditch cash accounting, the road forward is even steeper and blurry. And no city represents the conundrum more clearly than the one from which we narrate this story.

Bengaluru, which historically followed cash-based systems, had tried accrual-based accounting in FY18. But then, as per NITI Aayog, it couldn’t complete its transition successfully. So now, BBMP finds itself in a weird hybrid of both, which has created ambiguity around its recent financial statements.

It became difficult to ascertain the actual value of its arrears. More worryingly, BBMP doesn’t report tax write-offs despite state accounting manuals explicitly requiring it to. All of this made it mathematically impossible for the author of the CSEP paper to calculate how efficiently BBMP collects its taxes.

BBMP is still considered one of the early reformers in India. It is extremely worrying to think about all the other ULBs that are far more inconsistent in reporting their arrears.

What needs to change

The technical solutions aren’t particularly mysterious. Base rate revisions need to be small and frequent enough that they don’t trigger the kind of citizen backlash that one-time large jumps produce. Cities need to publish their full demand and arrears data annually. GIS mapping needs to happen regularly — every five years in fast-growing cities, not once a decade.

But the institutional problems are far harder.

None of the above happens reliably in a city without an elected council. None of it happens at scale without municipal corporations that control their own staffing and can hold their own staff accountable. None of it happens without ULBs that actually hold elections.

A change in the valuation method also doesn’t happen without the independence of the ULBs. It is a politically-sensitive topic among people who tie much of their wealth in land. And when local politics do flare up, state governments may try to appease people by suppressing the ULB.

These manifest as potholes in roads that remain unfixed for years, or drain overflows, or long waits for water. The ULBs have no capacity or freedom to actually solve these gaps. Property tax is not going to close them on its own. But it is one of the most direct, most locally accountable sources of urban revenue that exists. And it’s going backwards in real terms.

The world runs on a metal it can’t mine

There’s a metal that, almost like butter, melts when you hold it. It turns liquid at 29.76°C, well below the heat of your body. Take it in your hand, and it softens and pools into a silvery liquid puddle. Set it down on a table and it solidifies again.

This is gallium: element 31 on the periodic table. This strange metal that liquifies easily is also one of the most important materials in the world. It is inside every 5G base station, every LED screen, every military radar system, and increasingly, every fast charger and electric vehicle power converter on the planet. Without it, large parts of modern technology would simply stop working.

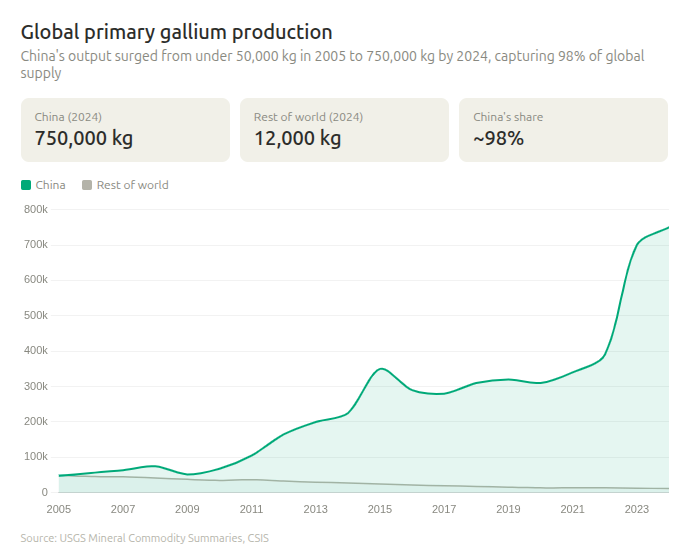

And a single country — China — produces 98-99% of the world’s supply. It has already demonstrated, twice, that it’s willing to cut the world off the metal.

The reign of silicon

Every piece of electronics you own needs silicon. Silicon is the bedrock material of the digital age, and it has been so ever since three physicists at Bell Labs built the first working transistor in December 1947.

Semiconductors

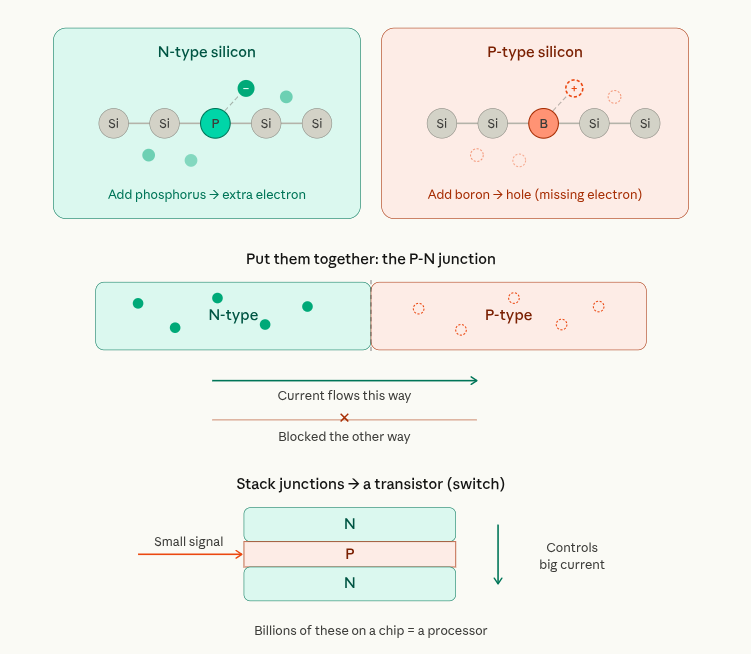

Silicon conquered the world because of one property: its ability to act as a semiconductor. Most materials are either conductors (they let electricity flow freely, like copper) or insulators (they block it, like rubber). Silicon, though, sits in between. It is sometimes a conductor; and sometimes an insulator. And crucially, one can control what it behaves like.

You can change how much electricity flows through silicon by adding tiny amounts of other elements, in a process called “doping”. Add a tiny amount of phosphorus, and you get extra electrons floating around. That turns it into “n-type” silicon — n for negative, because those electrons carry negative charge. Add boron instead, and you create little gaps where electrons should be but aren’t. Those gaps are called “holes,” and they tend to behave like positive charges “moving” through the material. Hence, this becomes “p-type” silicon.

What if you put n-type and p-type silicon next to each other? Well, those extra electrons from phosphorus leap for the holes created by boron. You get a junction; current can flow in one direction, but not the other. Now, if you are clever in how you stack these junctions, you can do all sorts of things with current. You can, for instance, create a transistor: a tiny switch that can flip on and off billions of times a second.

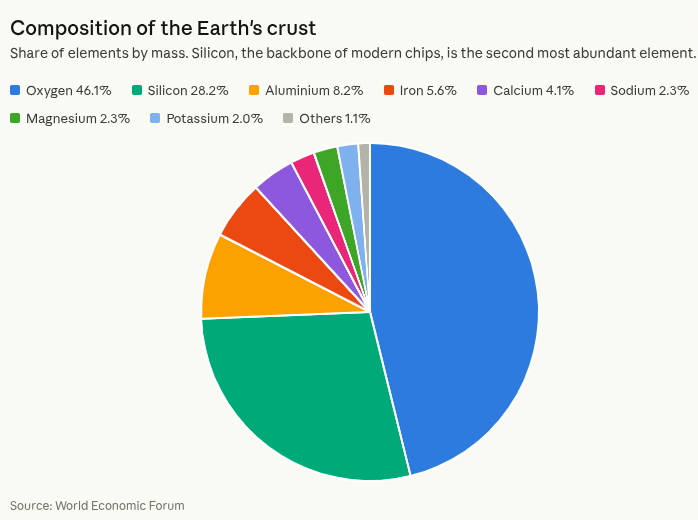

The first transistors used germanium. But silicon, we soon realised, worked even better than germanium. It could handle higher temperatures and was easier to find. It is, after all, the second most common element in the Earth’s crust, after oxygen.

From there, things moved fast. By the 1960s, engineers figured out how to cram multiple transistors onto a single chip. By the 1970s, entire processors could fit on a sliver of silicon. We were soon off to an exponential path, where we kept doubling the number of transistors in a chip every couple of years. As we did so, computers became smaller, faster, and cheaper at an exponential rate. The first Macintosh in 1984 had about 68,000 transistors. An iPhone today has over 15 billion.

Silicon made all of this possible. It was cheap, it was everywhere, and after decades of engineering, was incredibly well understood.

But silicon has a ceiling. And in the last decade or so, we’ve started hitting it.

Silicon’s ceiling

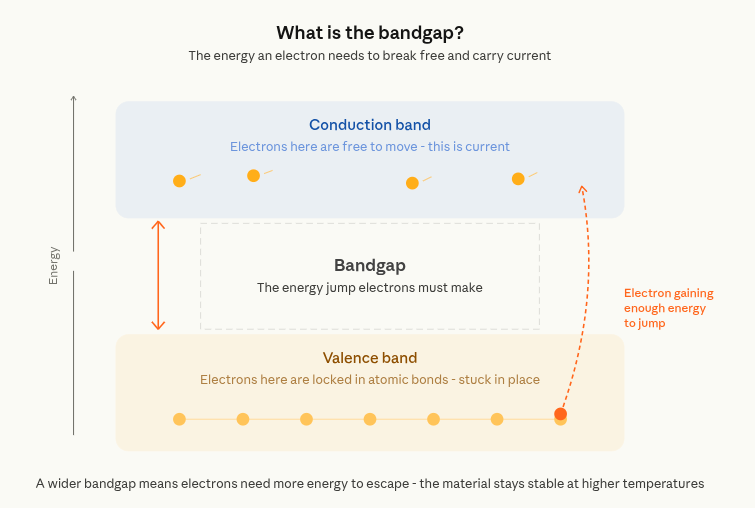

To understand the ceiling, you need to understand one concept: bandgap.

Inside any solid material, electrons sit in different energy states. Many are locked into the bonds that tie its atoms together. They hold the solid together, but that essentially leaves them stuck in place. But there are others, with more energy, that can break free of those bonds and move through the solid.

You can think of these as being two “bands” — the valence band and the conduction band. When current moves, it moves with electrons in the conduction band. What separates the two is energy. For an electron to jump from the top of the valence band to the bottom of the conduction band, it needs a specific amount of energy. That energy differential is called the “bandgap”.

Think of the bandgap as a wall inside the semiconductor. When the switch is “off,” electrons shouldn’t cross that wall.

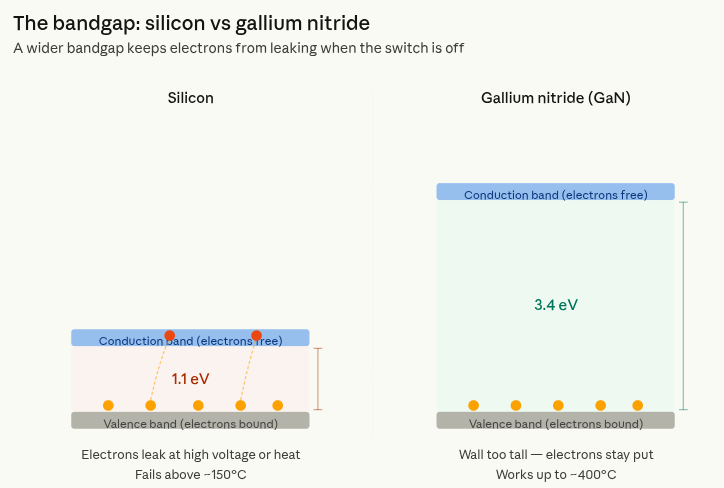

Silicon’s wall is short; just 1.1 electron volts (eV). For decades, this was fine. We weren’t pushing much voltage or heat through these chips. But then, our devices got more powerful, and that created problems. With the high voltages we were dealing with, electrons get enough energy to jump over the wall even when the switch was “off”. Current began flowing when it shouldn’t. The same problem appeared at high temperatures. That heat started giving electrons enough of a push to hop over the wall. Above about 150°C, silicon basically stops being a reliable switch.

For regular computing, this is manageable. You add cooling fans. You design around the constraints. But there’s an entire class of applications where silicon’s low wall has become a constraint.

Consider a 5G base station. It needs to constantly transmit and receive signals at frequencies above 3 GHz. Sometimes, it deals with frequencies above 30 GHz for millimeter-wave 5G. Meanwhile, silicon power amplifiers struggle above about 5 GHz, so the signal quality degrades.

Or consider a fast charger for your phone. The smaller and more efficient you want to make it, the faster the internal switches need to operate. Silicon switches are slow compared to what’s physically possible, and they waste energy as heat. This is why old chargers were heavy bricks that got burning hot.

We needed a higher wall. That’s why the world has turned to gallium.

Why gallium changes the physics

Gallium, by itself, isn’t a semiconductor. But combined with other elements, it creates compounds with extraordinary electronic properties. The two that matter most are gallium arsenide (GaAs) and gallium nitride (GaN).

GaAs has a bandgap of 1.4 eV — larger than silicon, which lets it handle higher voltages and temperatures. But its real edge is speed. Electrons move through GaAs much faster than through silicon, which means GaAs chips can process signals at extremely high frequencies.

Gallium nitride, meanwhile, is the more recent, and arguably, more transformative compound. Its bandgap is 3.4 eV, more than thrice that of silicon. GaN devices can handle electric fields that would destroy a silicon transistor. They can operate at temperatures up to 400°C, nearly thrice silicon’s limit. And its switches can turn on and off much faster. They also waste much less energy as heat, and therefore need less cooling. Things built with GaN, in short, are smaller, lighter, and more efficient.

A metal you cannot mine

But there’s a problem. For something so critical, gallium is remarkably hard to come by. It isn’t rare, exactly; gallium is actually fairly well distributed in the Earth’s crust. But it never appears in concentrations high enough to mine on its own.

Instead, gallium is a byproduct of alumina refining. Bauxite — the ore of aluminium — typically contains 30 to 80 parts per million of gallium. Midway through processing that bauxite into alumina, you get an aluminium-rich soup called “Bayer liquor”, which also contains small amounts of gallium. You can chemically extract the gallium from this soup.

This creates a unique supply dynamic: Gallium production is structurally parasitic on aluminium production. If the world suddenly needs twice as much gallium, you would have to ramp up how much alumina we produce.

But there’s another problem: not everyone that processes bauxite processes gallium.

How China cornered the gallium market

China produces almost all of the world’s gallium. They got there by building the world’s largest alumina refining industry, and then installing the equipment to extract gallium from the waste stream.

Most alumina refineries outside China never bothered with that. The economics historically didn’t justify it. The volumes were tiny, and it was just easier to buy from China. In fact, countries have actually been pulling out of the gallium trade. Germany stopped producing primary gallium in 2016. Hungary stopped in 2015. Kazakhstan in 2013. Ukraine likely stopped in 2022. The US has not produced primary gallium domestically since 1987.

Everyone let China take over nearly all of the world’s gallium supply. Then, Beijing reminded everyone that supply gives you leverage.

In August 2023, when the United States tried restricting chip exports to China, it imposed export controls on gallium and germanium. In December 2024, it escalated to a near-total ban on gallium exports to the US, one day after the US added 140 Chinese semiconductor firms to its “Entity List”. The ban included an “extraterritoriality clause”, that is, if a third country tried re-exporting Chinese gallium to the US, they would be in Beijing’s crosshairs too. By May 2025, gallium prices in Rotterdam had surged over 150% from pre-control levels.

Things de-escalated late in 2025, as part of the broader US-China trade truce negotiated between Trump and Xi Jinping, which prompted China to suspend the ban in November 2025. Exports to civilian US end-users resumed. But China only lifted the ban for a single year. Those restrictions can snap back at any time.

The scramble

It is only after the ban that the world has woken up to how important Gallium is.

The Pentagon has invested in several domestic gallium production projects. Even the most optimistic projections, however, suggest the US will produce only 10-15% of its national gallium consumption by 2030. In Europe, Greek company Metlen has invested $320 million to become the continent’s first commercial-scale gallium producer since 2016.

But it will take years and significant capital to get new sources of supply to production-grade quality — especially for semiconductor-grade gallium, which requires 99.99% purity or higher.

Until then, China’s chokehold continues.

India’s missed decade

India’s position in this story is particularly frustrating.

India is one of the world’s major bauxite producers. It has significant alumina refining capacity through NALCO, Hindalco, Vedanta, and ANRAK. Our bauxite deposits in Odisha contain at reasonable concentrations. And yet, as of today, India produces zero gallium.

In fact, NALCO even signed an MoU with the Bhabha Atomic Research Centre (BARC) in 2016 to develop technology for extracting gallium at its Damanjodi refinery in Odisha. A decade later, there is little to show for it. In that time, gallium prices have gone up almost 800%, from $274 to over $2,100 per kilogram. All we had to do, to ride this wave, was to process our own waste streams. Had we gotten to just 20 tonnes of annual production, say, in today’s prices, gallium revenue would be roughly ₹400 crore a year.

This inaction might be changing. In August 2025, NALCO announced plans for a 10-tonne-per-year gallium extraction facility. A prototype is expected in 8-9 months, and commercial production should begin within two years. If that timeline holds, India’s first gallium output will arrive sometime in 2027 or 2028.

It cannot come soon enough. India has big ambitions — we hope to make everything from semiconductors to defence systems at home. This project will need gallium. And unless we find solutions of our own, those ambitions could be held hostage by China.

Tidbits

India’s 60-year-old Income Tax Act, 1961 is officially dead. The new Income Tax Act, 2025, kicked in from April 1, replacing a law that had ballooned to 800+ sections and 47 chapters with a leaner 536 sections across 23 chapters. The biggest structural change: “Assessment Year” and “Previous Year” are gone, replaced by a single “Tax Year.” Tax slabs haven’t changed, but compliance gets easier. Other notable shifts: HRA claims now need landlord PAN, interest expenses can no longer be deducted against dividend or mutual fund income, and STT on futures is jumping from 0.02% to 0.05%. For retail F&O traders, that last one stings.

Source: Business Today

Car prices went up across the board from April 1. Tata Motors, JSW MG Motor, BMW, Mercedes-Benz, and Audi all hiked prices, ranging from 0.5% to 2% depending on the brand and model. The increases are driven by rising input costs, which have been compounded by the oil shock from the Iran war pushing up logistics and raw material prices. The auto sector had flagged these hikes weeks ago but they’re now effective.

Source: CNBC TV18IndiGo has appointed Willie Walsh, the current IATA Director General and former CEO of British Airways and IAG, as its new chief executive. He joins by August 3 after wrapping up at IATA. The appointment comes weeks after Pieter Elbers abruptly stepped down following the massive flight disruption fiasco in December, when thousands of cancellations exposed poor planning around pilot rest and duty rules. Walsh is known in the industry as “Slasher” for his ruthless cost-cutting, and his career includes steering BA through the 2008 financial crisis and engineering the BA-Iberia merger that created IAG. IndiGo shares jumped 9% on the news. The airline now operates 2,200+ daily flights with a 64% domestic market share, and the hire signals a push towards serious international expansion. Notably, both of India’s largest airlines (IndiGo and Air India) now have foreign-origin CEOs.

Source: CNBC

- This edition of the newsletter was written by Manie and Aakanksha.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

I read throughout second article.

Thanks for great article

On a separate note, is it possible to have two links for two articles that can be shared with others? All may not want to see through both articles…