When analysing any market, analysts usually start from the top-down i.e. the economy. Strategic analysts go even higher, looking at long-term trends and/or shifts in demographics, urbanisation, governance etc. That’s exactly where Akhilesh Tilotia started while working at Kotak. He wrote a book on the Making of India: Gamechanging Transitions (2015) to curate the number of transitions that were changing the Indian economy. However, it’s his own transition to working inside the government for three years that changed his perspective, some of which he has shared in his second book Through the Looking Glass (2021). The stint at the government-backed National Investment and Infrastructure Fund broadened his interaction with global investors and policy makers. While at NIIF, he would source bottom-up data from a start-up; he was so impressed with the work that he joined them as a co-founder of Thurro.

It’s this all-round view of India that makes a conversation with Akhilesh Tilotia interesting.

Private cost of public failure

The Making of India uses the term ‘private cost of public failure’ to indicate where the government or policy interventions have been unable to deliver basic hard and soft infrastructure services to expected standards. Power, roads, and water (bijli, sadak, paani) being the hard infrastructure, and education, health, and security (shiksha, swasathya, suraksha) being the soft. The government, either via policy or action, needs to be a credible player in public goods.

Tilotia argues that policy shapes markets, which shape prices, which in turn shape the society and its economy. In his book, he gives examples of how markets and prices have re-shaped many sectors. He hopes that Indian policymakers will continue towards freer prices. The

He admits that part of certain sectors, such as grains within agriculture, may find the move towards markets challenging. He argues that the majority of value in agricultural produce has indeed shifted to markets, with farmers moving increasingly to higher value-add horticulture, dairy, and meat. In the meantime, there are still logistics and credit challenges that could help the move to a more market-driven economy.

India’s demographic dividend has already been born. Between 23 and 25 million youth are joining the workforce every year, but pricing distortions in the labour market mean that many are not getting employed meaningfully. Tilotia believes that labour laws and manufacturing/export policies need to be more market-driven.

India’s urbanisation has been driven by the larger metros becoming agglomerations rather than an increasing number of cities. There is a missing middle in Indian cities. The larger cities have the lowest floor space index while being amongst the densest populated. Mass transport systems are being built even while the cities are expanding.

Governments need to balance stakeholder needs

The three-year stint in government made Tilotia realise the competing needs of various stakeholders that policymakers have to balance. The book points out that expert advisers don’t seem to appreciate the nuance of Indian democracy - politicians are somewhere in between the ‘trustee’ and ‘delegate’. If the ‘trustee model’ holds, the expert has a role and his advice is valuable in the discourse of shaping policies. If the ‘delegate model’ holds, the elected representative trumps the expert by simply pushing what his constituents want.

Experts and investors also tend to miss the fact that a politician’s pitch to his people are ‘orthogonal’ - where an expert looks at sectors, a politician looks at segments. “Where an expert sees a road, a politician sees the locality and community through which it passes; where an expert sees a school, the politician sees the youth; a gas cylinder may be an environmental project for an expert, it is a reason for the politician to speak to the women voters of his constituency.” Economic analysis reports calling for ‘reform wish-lists’ gloss over the “obvious fault lines of development (developmental, social, political), and do not call out contentious issues clearly.” They need to detail the principles to be followed in case of a trade-off, keeping in mind the voters.

Bottom-up data gives investors edge

After a full career of looking at the big picture, Tilotia finds the search for bottom-up data evidence for top-down views quite fascinating.

For example, in the first book he had postulated that ‘India will remain in the 20% tax-to-GDP ratio unless something alters dramatically.’ The rationale was -

Indirect tax (largely GST/ similar): With consumption to GDP at ~ 65% and assuming entire consumption bucket, comes to under GST/ similar tax, at say ~ 15% tax rate, the indirect tax-to-GDP ratio will be ~ 10%

If say 50% of the entire income (GDP) is put under the direct tax (many sectors like agriculture and segments of population below a certain income are exempt), and the average rate of tax is ~ 10%, this adds up to another ~ 5% of GDP. We already know from the number of tax filers that the proportion of taxable entities/ individuals is only about 5% of the population today.

The other 4-5% of the tax-to-GDP ratio comes from dividends, disinvestments, etc.

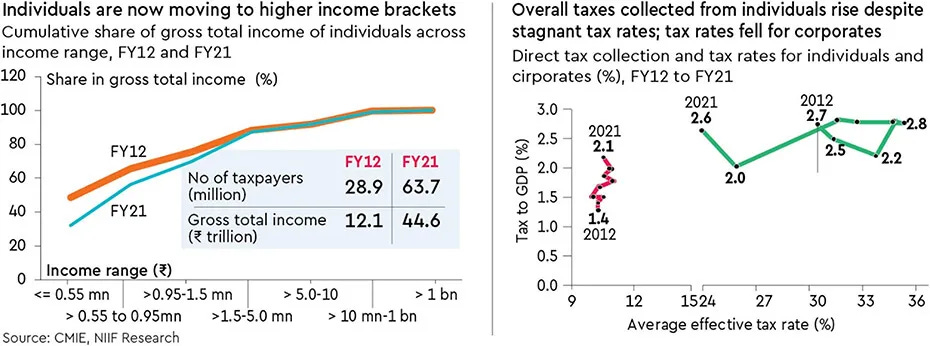

At Thurro, he can dive into the taxpayer data to see how India’s tax base is broadening slowly but surely. He points out that incomes show a move to higher brackets, even as more filers are coming into the tax net. The proportion of Gross Total Income (GTI)-to-GDP has increased from 24.2% in FY2012 to 35.1% in FY2021. Overall direct tax-to-GDP ratio has gone up from 4.1% of GDP to 4.9% over FY2012-21.The number of filers has grown from 31.3 million in FY2012 to 67.6 million in FY2021, and closer to 90 million more recently.

Generalist dot-joiner perspective on investing in India

The first conversation with Akhilesh Tilotia was intentionally an overarching one to get a broad perspective from someone who had approached investing in India from multiple perspectives. Hopefully, this conversation serves as an introduction to such a multi-perspective. We hope to build on this to go deeper into select aspects in the future.

We hope you are enjoying our “Investing in India” series and would love to hear your thoughts and suggestions. Feel free to drop us a comment anytime!

See you next time!

| A guest post by

|

Where Can I get the Blog format of this Interview ?

Some tech feedback:

It’s not playing on Apple Podcasts. Have tried on AirPods, a Bluetooth speaker. Other podcasts are working.

Please try and fix. Sounds like a great episode.