Amidst the ruins of Jaypee Group

And the hunt for its scraps

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Amidst the ruins of Jaypee Group

Why MasterCard is investing $1.8 billion in a crypto company

Amidst the ruins of Jaypee Group

Last week, the NCLT approved Adani Enterprises’ ₹14,535 crore bid to acquire Jaiprakash Associates (JAL), the flagship company of the Jaypee Group. Five days later, Vedanta moved the NCLAT to block the deal, calling it a “commercial conspiracy“. It says its bid was worth more.

For anyone who followed Indian markets during the infrastructure boom of the 2000s, the name Jaypee needs no introduction. This was the group that built the Yamuna Expressway, hosted India’s only Formula 1 races, and became the country’s third-largest cement producer.

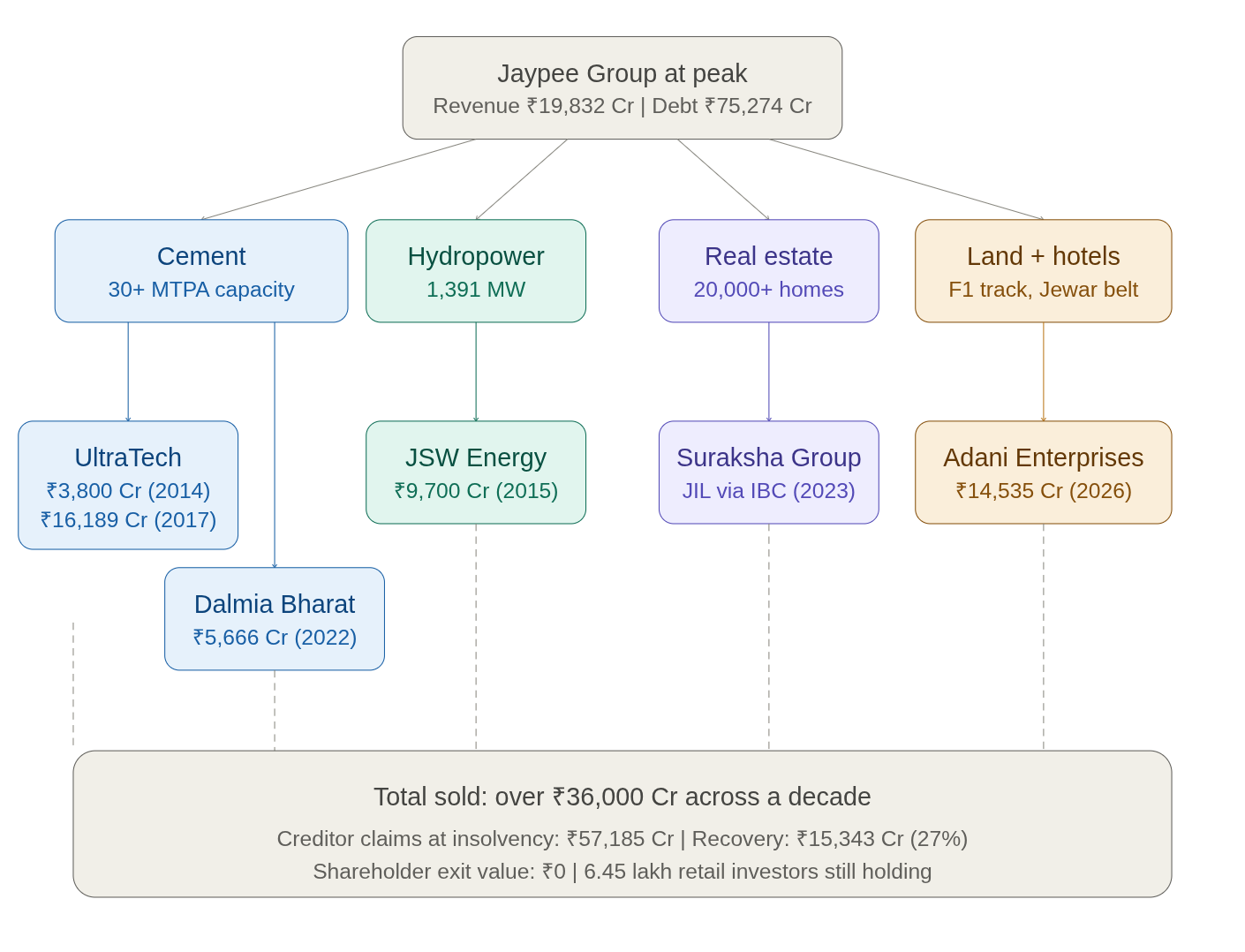

And JAL was the group’s biggest core. At its peak in FY2014, JAL reported consolidated revenues of ₹19,832 crore. The stock touched ₹324 in January 2008.

But today the stock trades at ₹2.40.

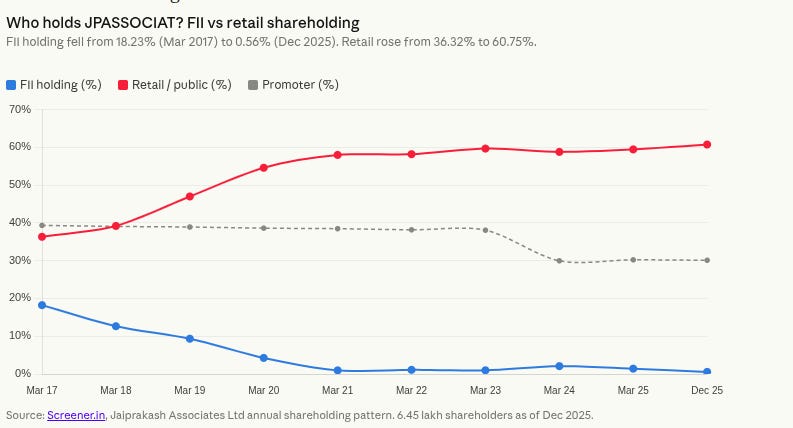

At insolvency, the company disclosed to the exchange that the exit price for existing shareholders is nil. The shares will be cancelled, and the company will be delisted, but 6.45 lakh shareholders still hold its stock. And most of them are average retail investors rather than institutions.

How did a company this large end up here? What are Adani and Vedanta fighting over? And what happens to the people still holding a stock that’s heading to zero?

Temples of modern India

The Jaypee Group had fairly modest beginnings, but its rise was meteoric.

Jaiprakash Gaur was born in 1931 in a village in Bulandshahr, Uttar Pradesh. He finished a diploma in civil engineering from what is now IIT Roorkee in 1950, and spent a few yea₹in the UP Irrigation Department. In 1958, he left to become a civil contractor on his own. His starting capital was ₹10,000 (roughly ₹10 lakh in today’s money, adjusted for inflation).

In over two decades, he built his company into India’s premier hydropower builder. He executed 13 projects simultaneously across six states and Bhutan, including projects like The Tehri Dam, Vishnuprayag, Baspa-II, and so on. Jaypee’s projects encompassed 27% of the country’s installed hydropower capacity — no other private firm came close.

Then came India’s post-liberalisation infrastructure boom. And Gaur decided hydropower wasn’t enough.

Through the 2000s, Jaypee grew from a construction company into a conglomerate, adding businesses at a blindingly-fast pace.

Cement came first, and why wouldn’t it? Jaypee already consumed enormous quantities of cement for its dam and construction projects, so it might as well make its own. By the early 2010s, the group’s cement capacity exceeded 30 million tonnes per annum, making it India’s third-largest producer.

After that came real estate, which, of course, also uses cement. Through subsidiaries Jaypee Infratech and Jaypee Greens, the group launched massive residential townships in the Noida-Greater Noida belt. These developments sat in the path of what was clearly going to be one of India’s fastest-growing urban corridors, right next to the Yamuna Expressway that Jaypee itself was building. Tempted by that proposition, tens of thousands of families booked homes.

The Yamuna Expressway, commissioned in August 2012, was the showpiece. 165 kilometres of six-lane, access-controlled concrete road connecting Noida to Agra, at the time the longest such expressway in India. Jaypee also had their own thermal power plant at Nigrie in Madhya Pradesh, on top of the existing hydro capacity. It also built hotels in Delhi-NCR, Mussoorie, and Agra.

And then, in 2011, it made the bet it’s probably most infamous for: the Buddh International Circuit in Greater Noida, that hosted India’s first Grand Prix in October that year.

By FY2014, JAL alone reported consolidated revenues of ₹19,832 crore. Its success was emblematic of how Jaypee Group became one of the defining conglomerates of India’s infrastructure age.

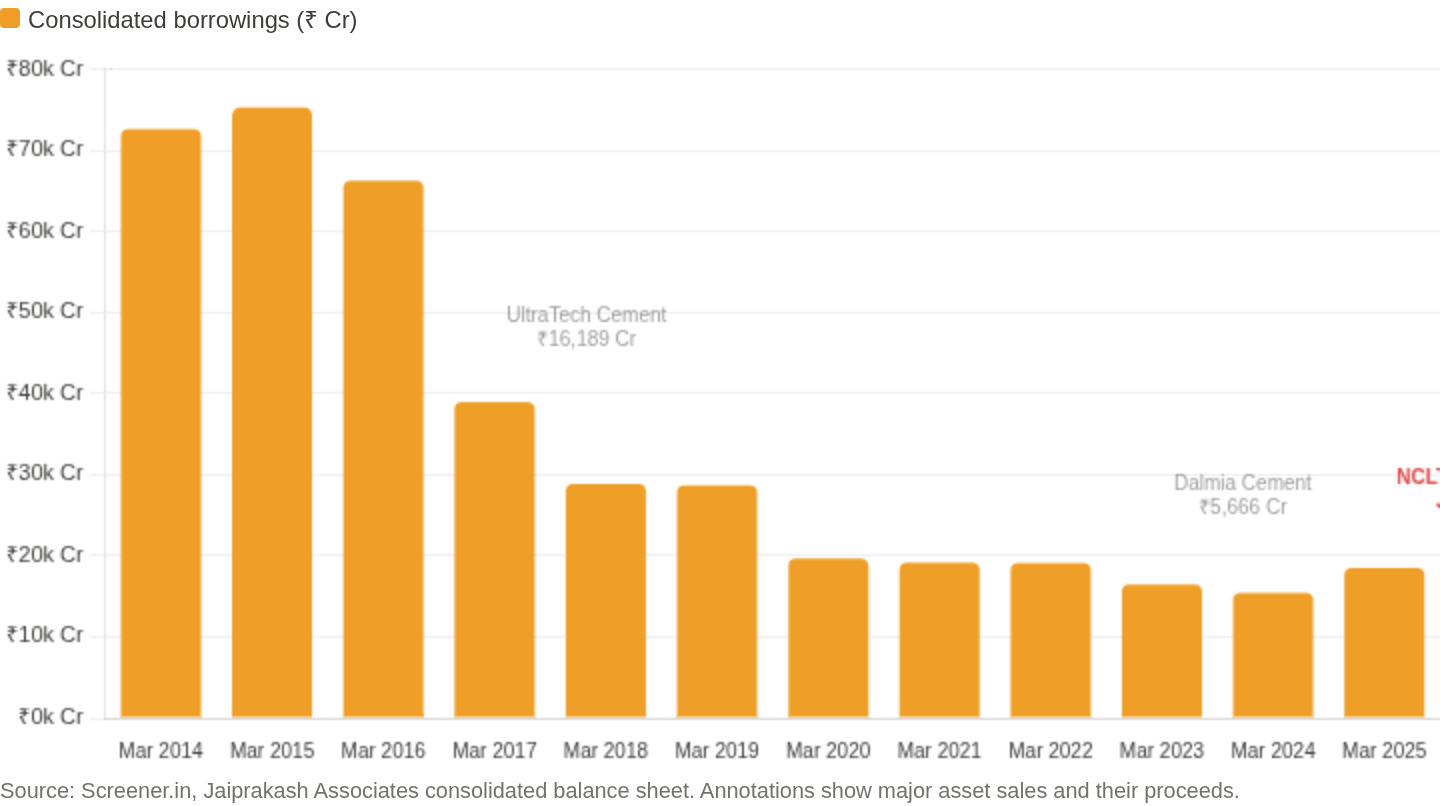

But in that same year, JAL was also carrying ₹72,599 crore in consolidated borrowings. That number was still climbing, and would eventually grow big enough to unravel everything.

The debt trap

Jaiprakash Associates borrowed too much, too fast, from too many lenders, for too many projects at the same time. Everything else, the real estate delays, the regulatory troubles, the macro shocks, sits on top of this house of cards.

Every new business required its own pool of capital, and all of it came from debt. Hydropower projects cost ₹5,000-10,000 crore each and take years to generate revenue. The Yamuna Expressway alone was ₹12,000+ crore. Cement plants, real estate townships, and hotels were no joke either. The F1 circuit had no clear revenue model established after the races stopped.

What makes it worse is the timing of it all. All of these projects were in various stages of construction simultaneously, all consuming cash, none generating proportionate revenue yet. JAL’s consolidated borrowings hit ₹72,599 crore in March 2014, rising to ₹75,274 crore by March 2015, which was the peak.

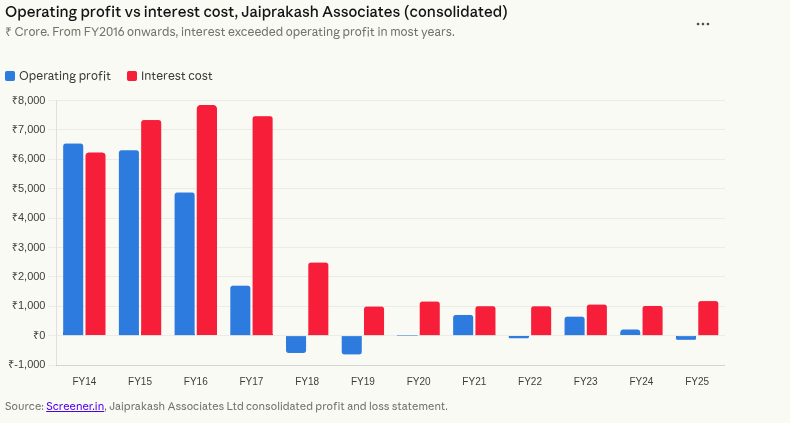

At that level of debt, interest costs alone were ₹6,233 crore in FY2014. By FY2016, they had risen to ₹7,847 crore, roughly ₹21.5 crore per day. Every single day, before Jaypee sold a bag of cement or collected a toll, it owed its lenders ₹21.5 crore in interest alone.

The operating profit in FY2016 was ₹4,871 crore, while the interest bill was ₹7,847 crore. The company was earning less from its businesses than it was paying to service its debt.

And then, when the foundation was already unstable, the castle began collapsing one by one.

First, the real estate projects stalled. Buyers who had paid EMIs for years weren’t getting their flats. Construction slowed, then stopped at several sites. Regulatory disputes with YEIDA over land allotments and environmental clearances added to the paralysis. Homebuyers had to resort to the court for settlement.

Second, the hydropower projects overran. Building hydro projects in rocky, inaccessible terrains like the Himalayas is extremely difficult. Several projects saw cost escalations of 40-60% over original estimates. Tariff approvals from state regulators lagged years behind, and revenue that was supposed to service the loans didn’t arrive on schedule.

Third, the macro environment turned multiple times against Jaypee. The 2008 crisis tightened credit, and the 2013 taper tantrum weakened the rupee and pushed up imported input costs. What’s more, after the 2G spectrum scam and coal block allocation controversy, regulatory eyes keenly began eyeing large infrastructure conglomerates like Jaypee.

The result was a company that had built genuinely valuable assets on top of prime land, but couldn’t generate enough cash. From FY2015 onwards, JAL reported losses in almost every single year. It was racking up debt faster than any F1 car.

Sold for parts

By the mid-2010s, lenders were pressing Jaypee to sell assets and reduce debt. What followed was a decade-long fire sale of the group’s most valuable operating businesses, each one meant to save what remained after.

The dismantling took a decade. UltraTech bought the Gujarat cement plants in 2014, and then came back in 2017 for most of the rest of its cement infrastructure, sold at ₹16,189 crore. JSW Energy, meanwhile, took two hydropower projects for ₹9,700 crore in 2015. Dalmia Bharat picked up the remaining cement and clinker capacity in 2022 for ₹5,666 crore.

Jaypee Infratech, the subsidiary behind the Yamuna Expressway and Noida’s real estate, went to Mumbai-based Suraksha Group in 2023 after four rounds of bidding over six years. Yet, over 20,000 homebuyers are still waiting for their flats.

But, none of those deals helped save any part of the conglomerate.

After each sale, the remaining businesses continued to rake up losses, and the interest kept accruing. So, the debt had actually compounded faster than the assets could be sold. The total proceeds across all these sales amounted to over ₹36,000 crore. Yet when the NCLT admitted JAL into insolvency, creditors had filed claims of ₹57,185 crore.

So, despite all of that, with not much left to sell voluntarily, JAL was forced to declare insolvency in 2024.

The winner takes it all

What was left inside JAL by the time it entered the NCLT?

Primarily, there was a huge land bank that sat around the upcoming Noida International Airport. It contained Jaypee Greens, portions of Wishtown, the Sports City complex, and so on. When that airport opens, this corridor could become very valuable. On top of that, there is the Buddh International Circuit, 12 incomplete residential projects, five hotels, and stakes in Yamuna Expressway tolling.

All of this still had the potential to be prime real estate. And all the players vying to bid for the scraps knew it. Initially, five bidde₹showed up: Adani Enterprises, Vedanta, Dalmia Bharat, Jindal Power & Steel, and PNC Infratech. By the final round, it was down to Adani and Vedanta.

Vedanta offered ₹17,000 crore in headline value, but spread payments over five years. Adani offered ₹14,535 crore, a lower number on paper, but around ₹6,000 crore of it was upfront cash, with the rest payable within two years.

Think about it from a lender’s perspective. After waiting years to get paid and taking massive write-downs, for you, money now would be worth more than a larger number promised later. It’s those promises that had burned you earlier.

So, the Committee of Creditors, led by NARCL, which had acquired JAL’s stressed loans from the SBI-led consortium, approved Adani’s plan with an overwhelming majority. This committee weighs plans across multiple dimensions, not just headline value, but cash structure, feasibility, the bidder’s ability to actually run the business, and speed of implementation.

Vedanta doesn’t accept this decision, though. Its challenge at the NCLAT rests on three arguments.

They said even after adjusting for the fact that their payments were spread over five years, the total value of their offer was higher than Adani’s by roughly ₹500 crore on a net present value basis. In other words, Vedanta believes lenders would have received more money in real terms under its plan, even accounting for the delay.

Secondly, Vedanta submitted a revised offer on November 8, 2025, raising upfront cash to approximately ₹6,563 crore and adding ₹800 crore in equity infusion — essentially matching Adani’s cash advantage. It says this was ignored. But the lende₹say it arrived after the bidding window closed, and accepting it would mean reopening the entire process.

Lastly, Vedanta claims it was never given reasons for the rejection of its bid, nor a chance to clarify its proposal.

The NCLT dismissed Vedanta’s objections on March 17 and approved Adani’s plan. Vedanta moved the NCLAT five days later.

Where this leaves everyone

The lenders recover roughly ₹15,343 crore against claims of ₹57,185 crore, a 73% haircut, but the first real money they’ll see from Jaypee in years.

There isn’t enough to fully pay even the secured lenders, while the equity shareholders— most of whom right now are retailers — get nothing. Institutional investors seemed to have escaped the fallout on time.

Adani, meanwhile, gets a portfolio whose value hinges on the new Noida airport and the completion of stalled projects. Of course, by virtue of owning UltraTech, Aditya Birla has a large chunk of JAL’s cement business. Vedanta gets its day in court.

What happens next depends on a bench in Delhi. But this is definitively the end of a conglomerate that started with humble origins.

Why MasterCard is investing $1.8 billion in a crypto company

A little more than a week ago, MasterCard announced it would acquire BVNK, a London-based stablecoin infrastructure company, for up to $1.8 billion.

Here’s what BVNK does: say a company in the US wants to pay a supplier in Singapore using stablecoins, but the supplier only wants to receive Singapore dollars in a normal bank account. BVNK handles the translation, converting between regular currencies and stablecoins. It does so across 130 countries, on every major blockchain.

This is the game Mastercard — a company whose business model should, in theory, be existentially threatened by crypto — is entering. Consider that: MasterCard makes money by sitting in the middle of every payment. Stablecoins were designed to eliminate the middle entirely.

And yet, this wasn’t a sudden pivot. MasterCard has been building toward stablecoins for nearly a decade. It filed its first blockchain patents in 2017. It acquired a blockchain analytics firm in 2021, and then piloted stablecoin settlement with USDC that same year. By 2025, it had enabled four stablecoins on its network, and had launched a ‘Crypto Partner Program’ with over 85 companies.

MasterCard isn’t alone. Visa, too, has been settling transactions in the stablecoin USDC since 2023 and now runs over 130 stablecoin card programs across 40 countries. Stripe spent $1.1 billion buying Bridge, a stablecoin platform whose clients include SpaceX. PayPal went a step further — it launched its own stablecoin, PYUSD.

That is, the world’s biggest payment companies are spending billions to integrate the very technology that was supposed to make them obsolete. What do they see that we don’t?

The answer becomes clear once you understand what a payment actually is — and how card networks and stablecoins solve different parts of it.

How card networks managed payments

Imagine you’re at a store. You tap your card to pay, and the terminal says “approved.” It’s instant; the payment is done.

But curiously, no money actually moves from one place to another.

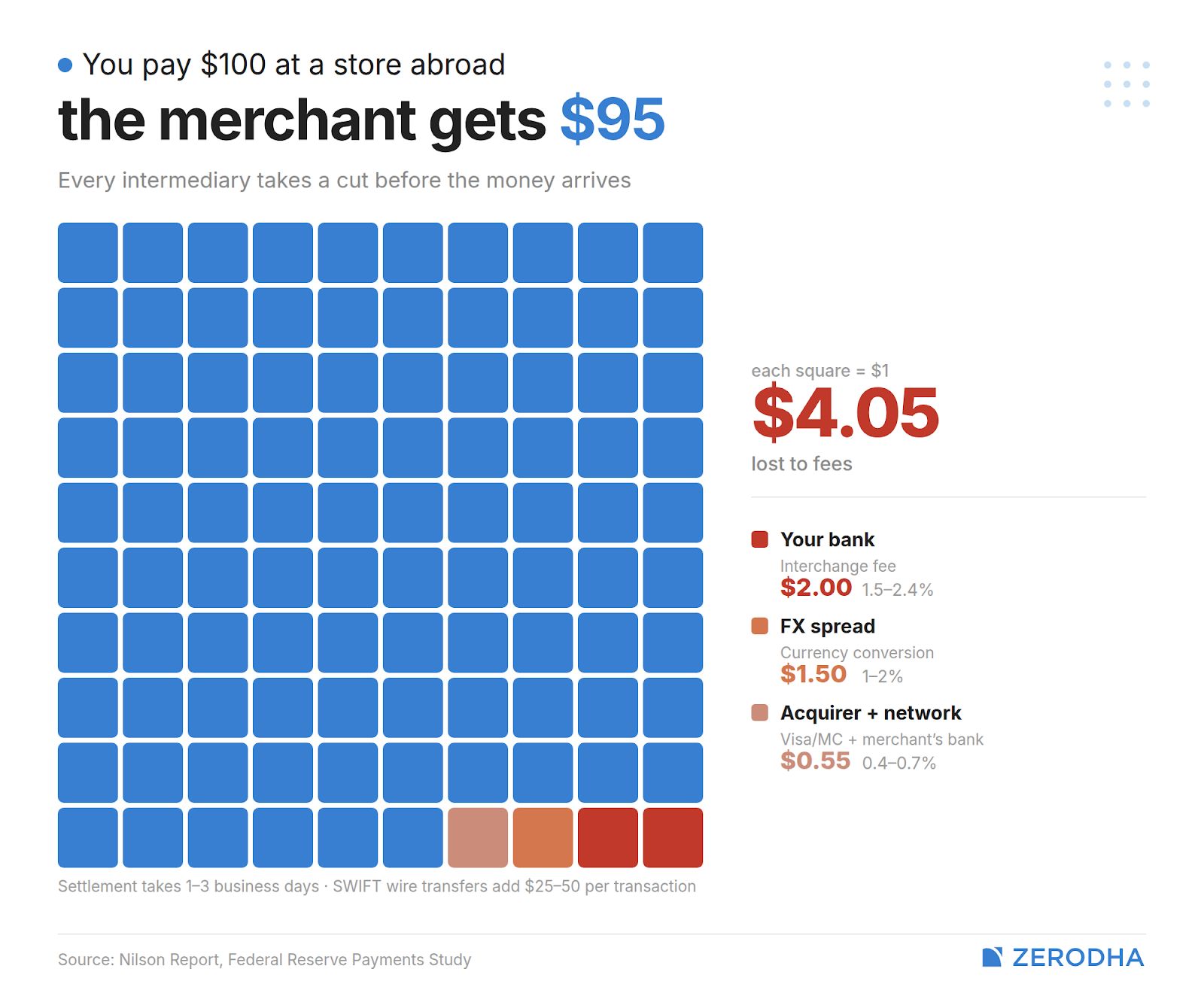

What’s happened, instead, is that your bank has sent a message — through the card network — confirming that you’re good for the payment. The merchant has received a promise, backed by the network’s rules, that the money will come. But it doesn’t actually move yet. The actual cash only settles one to three business days later, when banks clear their obligations in batches.

Cross-border transactions are even slower, since they come with a currency conversion layer, and often route through three to five correspondent banks, stretching settlement further and adding fees at every hop.

As this happens, every party in this chain takes a cut. When a merchant accepts a card payment, they don’t receive the full amount — they lose roughly 2–3% of it. Most of that goes to the consumer’s bank as a fee called “interchange”. Think of it as the bank’s reward for lending the consumer money and taking on the risk. And if the payment crosses a border, another 1–2% gets added in currency conversion markups. International wire transfers are even worse: they cost $25–50 per transaction, along with exchange rate spreads on top, and take as many as five business days of waiting.

If that sounds expensive, well, it is.

That money goes into funding an entire ecosystem, down the line. When you pay with a credit card, you’re borrowing money. Your bank is extending you unsecured credit at the point of sale, which is interest-free for up to 45 days. The card may also offer rewards. In just the single year of 2022, for instance, America’s six largest issuers paid out $67.9 billion in reward redemptions. Airlines, hotels, and retailers have built entire loyalty ecosystems — miles, cashback, lounge access — funded by this interchange revenue.

It also funds a safety net. Many cards run zero-liability fraud policies — that is, you don’t pay for any unauthorised transactions charged on your card. Similarly, “chargebacks” let you dispute a charge and get your money back.

In other words, the 2–3% a merchant pays isn’t just the cost of moving money from A to B. It’s funding an entire ecosystem of credit, rewards, fraud protection, and consumer trust that sits on top of the payment.

At least for now, though, none of that exists natively on stablecoin rails.

How stablecoins change things

A stablecoin takes a fundamentally different approach.

Where card networks separate the approval from the actual movement of money by a few days, with stablecoins, that gap is zero.

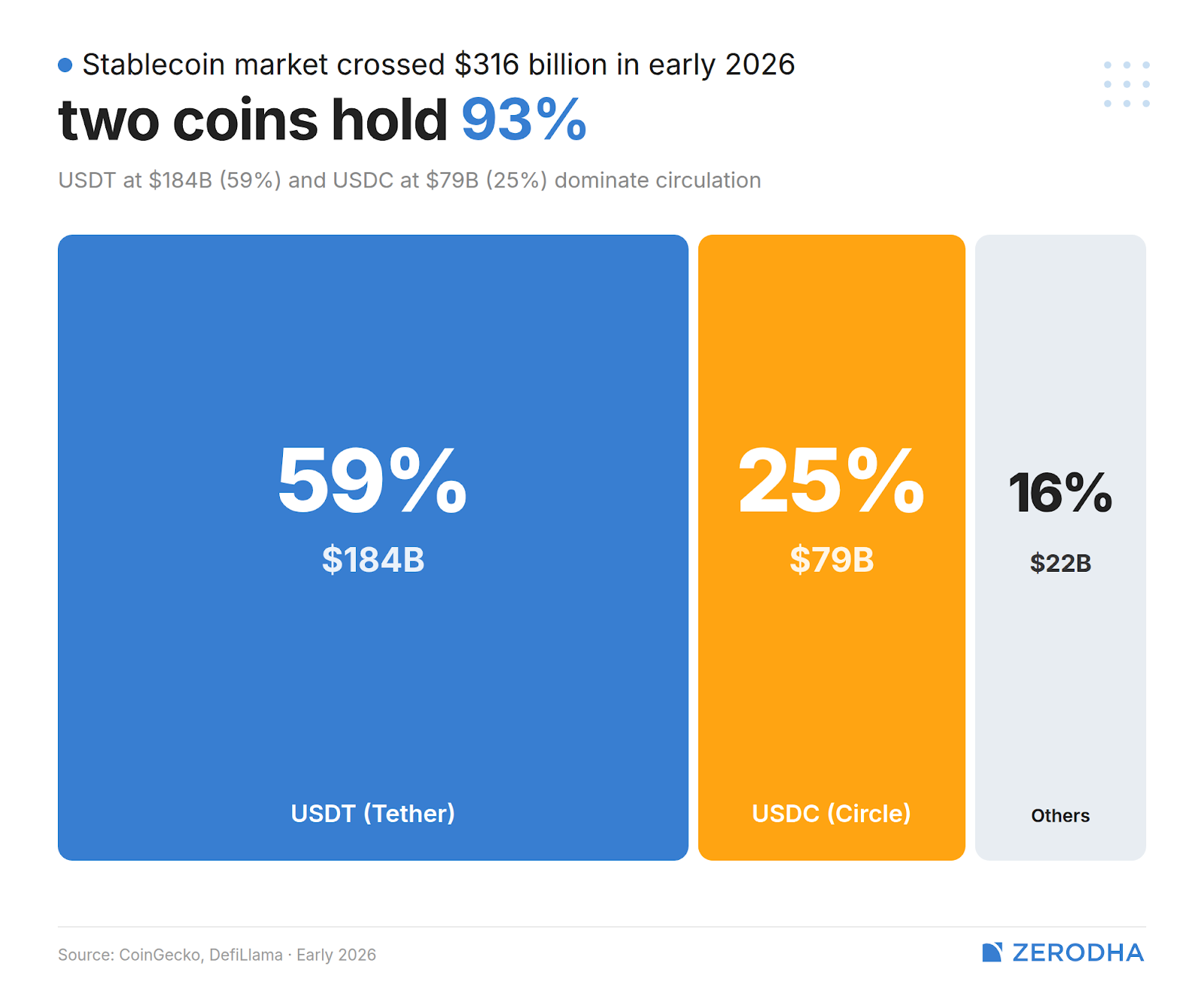

A stablecoin is a digital token pegged 1:1 to a fiat currency — almost always the US dollar — and backed by reserves of cash, Treasury bills, and money-market instruments. The two dominant stablecoins are Tether’s USDT and Circle’s USDC. Together they account for 93% of the stablecoin market, which stood at $316 billion in total circulation as of early 2026.

That peg is maintained through arbitrage. If USDT trades at $0.99, for instance, traders buy it cheaply and redeem it from Tether for $1 of underlying reserves, pocketing the difference. This buying pressure pushes the price back to $1 — a simple correction, provided the reserves actually exist.

Of course, this can also go very wrong. Terra/UST’s $45–50 billion collapse in 2022 — an algorithmic stablecoin with no real reserves — showed what happens when they don’t.

When you send USDC to someone, the token moves directly from your wallet to theirs on a blockchain. The blockchain automatically handles verification, and as the token moves, settlement is completed. There’s no promise to pay later. Unlike in a card network, money instantly changes hands.

This is also much cheaper. A cross-border card payment that costs 3–4% and settles in days can happen on stablecoin rails for a fraction of a cent, and within seconds. The World Bank pegs the global average cost of sending a $200 remittance at 6.5%. Stablecoins on low-cost chains can do the same thing for under 1%.

But here’s a caveat: stablecoins are only cheaper if you don’t need what the rest of the traditional card bundle provides. If the merchant still wants fiat conversion at the end, if the consumer needs customer support, if there’s an error that needs reversing — new intermediaries and new costs reappear. And if something goes wrong — a fraudulent charge, tokens sent to the wrong address — there’s no chargeback, no bank to call. Stablecoin transactions are irreversible by design.

That is, stablecoins aren’t a magical zero-cost rail. They come with a different cost structure. They strip away the trust layer to make settlements radically more efficient. But credit cards had created an array of services around that inefficiency, and stablecoins have none of that either.

Where each system wins

For everyday consumer purchases — the tap at the store, or an online checkout — card networks are simply better. It’s not even close.

Stablecoins simply don’t have product-market fit here. No consumer is going to convert their salary into USDC to buy groceries. They’re unlikely to forfeit credit, rewards, and fraud protection. Card networks may not be faster or cheaper at moving money, but their trust layer, along with the sheer familiarity they’ve built over decades, is something stablecoins haven’t even begun to replicate. Executives at both Visa and MasterCard have said as much publicly.

But for cross-border settlement, B2B payments, remittances, and treasury operations, stablecoins win. When the hard problem is moving the money itself — across banking hours, across jurisdictions, through intermediary chains — stablecoin economics are far better. That’s clear form the data. Cross-border B2B stablecoin payments surged from under $100 million monthly in early 2023 to over $6 billion monthly by mid-2025.

But there’s an interesting space in between. Consider a Shopify merchant in India, selling to a customer in the US. The customer pays with a card. Card networks win that checkout.

But the merchant receives funds days later, after conversion fees eat into the margin. If the merchant could instead receive stablecoins — settling in seconds, at a fraction of the cost — the consumer experience would stay the same, while the merchant’s economics would transform. This overlap zone — online commerce, marketplaces, merchant settlement, payouts — is where the neat division starts to blur.

How they actually interact

This is where the MasterCard and Visa deals start making sense. In practice, card networks and stablecoins don’t compete in a single way — they layer together differently depending on who needs what.

Here’s one configuration: stablecoins are completely invisible to everyone except the banks. You tap your Visa card, the merchant sees a normal Visa transaction, the checkout experience is unchanged. But behind the scenes, instead of your bank and the merchant’s bank settling through traditional interbank clearing over the next few days, they instantly settle in USDC on a blockchain.. Visa launched exactly this in the US in December 2025, and reported a $3.5 billion annualised stablecoin settlement run rate.

Let’s try something different. Now the consumer holds stablecoins — say, USDC in a crypto wallet — and wants to spend them. They can use a MasterCard-branded card linked to that wallet. When they tap to pay, the stablecoin converts to fiat at the point of sale. The merchant still experiences a completely normal card payment. MasterCard still collects interchange. But the consumer just spent crypto. This is what the MetaMask and OKX card partnerships do.

Here’s another. Now the merchant wants stablecoins. A customer pays with a regular card, but the merchant receives stablecoins instead of fiat — instantly.

MasterCard’s $1.8 billion bet on BVNK is about owning the infrastructure that makes all three models work.

Of course, you can pull out of the card network entirely. A customer can just send stablecoins directly from their wallet to the merchant’s wallet. This is the pure crypto vision. But it only works when both sides are comfortable with irreversible transactions and don’t need fraud protection or chargebacks. But most aren’t. Without the merchant acceptance network, the consumer trust infrastructure, and the dispute resolution machinery, this model hasn’t scaled beyond niche use cases.

Conclusion

The simplest way to understand this entire story is one sentence: stablecoins changed the settlement layer of payments, but not the trust layer. Card networks own the trust layer of merchant acceptance, fraud protection, credit facilities, rewards ecosystems and dispute resolution. So the future isn’t cards or stablecoins. It’s cards with stablecoins underneath, stablecoins with cards on top, and in a narrower set of cases, stablecoins without cards at all.

Where you stand on that spectrum depends on what kind of payment you’re making. India is a good example. UPI has already solved domestic payments with near-zero fees and instant settlement — stablecoins add nothing there. But India is also the world’s largest remittance recipient, and those corridors still cost 4–6%. The stablecoin opportunity may not be at the chai shop, but one certainly exists in the correspondent banking system that taxes every rupee sent home.

The reason card networks can ride this shift, rather than be destroyed by it, is that commercially relevant stablecoins are not the decentralised, anti-intermediary money that crypto originally promised. USDT and USDC are issued by centralized companies that can freeze wallets, control supply, and comply with law enforcement. The US GENIUS Act, signed in July 2025, subjects stablecoin issuers to bank-like regulation.

All that’s decentralised is the settlement infrastructure. But the institutions running them are familiar.

Tidbits

NHAI’s Raajmarg Infra Investment Trust lists on the exchanges today. It’s India’s largest highway InvIT offering ever, having raised Rs 6,000 crore at Rs 99-100 per unit. The IPO was subscribed nearly 14x, with strong QIB demand at 19x. It’s part of the government’s broader asset monetisation push, where NHAI sells toll rights to investors and recycles the capital into building new highways.

We also broke the IPO down in a recent Daily Brief episode.

Source: BloombergIndia’s strategic petroleum reserves are only 64% full and cover just 9.5 days of crude oil needs, the government revealed in a Rajya Sabha reply on Monday. That’s 3.37 million metric tonnes out of a total 5.33 MMT capacity across three underground caverns in Vizag, Mangaluru, and Padur. On adding commercial stocks held by oil marketing companies, total cover goes up to 74 days.

Source: Business TodayHDFC Bank has hired external law firms to examine ex-chairman Atanu Chakraborty’s resignation letter, which cited concerns over “values and ethics.” As per some sources, the rift may partly involve client losses from Credit Suisse AT1 bond mis-selling.

Source: Bloomberg

- This edition of the newsletter was written by Aakanksha and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉