The three bodies that couldn’t kill Airtel

Plus: How NRIs are being called to defend the rupee

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The three bodies that couldn’t kill Airtel

How NRIs are being called to defend the rupee

Today’s edition is slightly different from the ones we’ve done before.

Our first story today is authored by Rohin Dharmakumar, CEO of The Ken, one of the best independent business journalism publications in India. It is based on their deep-dive into the history of Airtel, which was released as part of their long-form podcast series Intermission. If you have the time, we highly recommend watching it in full.

They also have a cool companion site for the episode containing charts and visualisations created by Anuj Debnath, The Ken’s data visualisation journalist.

The three bodies that couldn’t kill Airtel

Picture Sunil Mittal, the founder of Airtel, surrounded by three very powerful planets orbiting him. Physics has an analogy for this situation, called the three-body problem. You might be aware of it through the hit book franchise of the same name by science-fiction author Liu Cixin, and the adapted Netflix show.

The three-body problem says that when three bodies are orbiting each other in space, it is virtually impossible to predict their path. Eventually it starts to become chaotic, and they crash into each other. In his book, Liu Cixin described an alien race that lives under three suns, making their world’s climate unpredictable and forcing them into brief windows of order punctuated by devastating collapse.

Swapping for a different setting, Liu could have just as easily been describing India’s telecom sector. For 30 years, Airtel has lived inside exactly the chaos that has fogged the industry, and changed it.

In our real world, the three bodies are regulation, technology, and competition. Airtel has been hammered by India’s regulators, by every wave of telecom technology you can think of, and by its biggest competitor, Reliance, twice. Yet, it has managed to come back stronger each time.

But first, why was the fight even worth it?

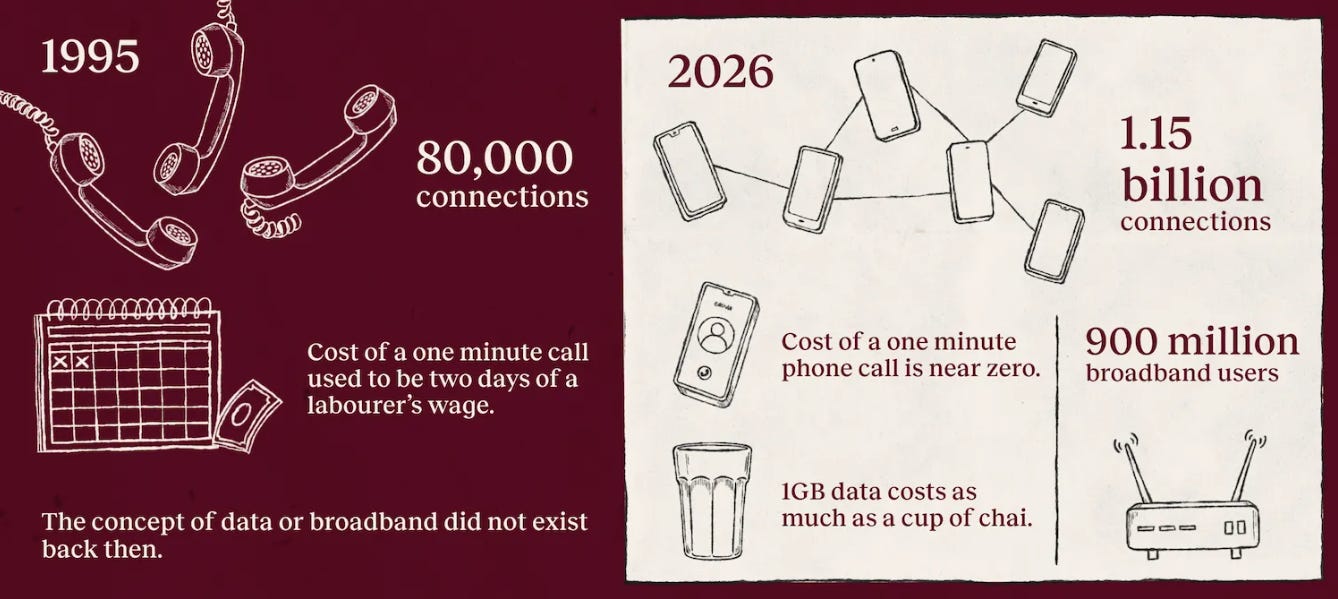

See, telecom is fundamentally a regulated oligopoly. In any market anywhere in the world, this sector typically has at most three or four players. It is essentially a business where the regulatory moat is disguised as a license, and those with that license sell an incredibly addictive and recurring service. Nobody cancels their mobile number. You might cancel your OTT subscription, you might decide not to order from a quick-commerce platform, but you’re never going to cancel your number.

I got my number from Airtel in 2001. That’s 25 years of paying Airtel bills every month, and I could buy a very good car today with what I’ve spent to keep my one number. Once you build that pipe, you have the optionality to sell many services over it, so the business compounds on itself.

Meanwhile, high fixed costs act as a moat against new entrants, and that’s paired with nearly zero marginal cost. Airtel’s incremental EBITDA on a new 4G customer is north of 80%.

In some ways, it’s the holy grail of business models. That’s why Airtel was always going to be on the radar of very powerful entities.

The first body: regulation

Let’s start with the first body, regulation.

Indian telecom regulation is a shape-shifting reality. One of the truths of Indian regulation of any kind is that everything is always open to subjective interpretation. Who knows the pattern until it’s settled in a court, and who knows whether that’s true until it’s settled at the Supreme Court?

To start with, in the mid-1990s, the state awarded licenses in four cities based on qualitative points; Airtel almost lost out before lucking into Delhi. That was entirely subjective, almost as if it were a beauty pageant — which is exactly what industry insiders called this process. And naturally, it was prone to flip-flops.

Then, for the expansion of the next 18 cities, auctions were introduced. They were more objective, and for the first time, spectrum was unbundled from licenses and priced separately. But the payment schedules were heavily front-loaded: you were forced to match the highest bid, and roughly 57% of the value was due in the first three years, even though building networks took much, much longer.

That combination broke companies. By 1999, the whole sector was on the verge of collapse. Every company had defaulted on its license fees. One of the former CEOs I spoke to called it a night with no end. The flaw in the system was bidding fixed license fees, because nobody had a clue how much money they would make. Even in the best case, you were broke before you got rich.

Then, the same year, the government announced a new telecom policy, NTP, which was a welcome change. It was a recognition of the fact that if every company in the sector went under, there would be nobody left to offer telephony. The NTP helped make a shift from a fixed license fee to a revenue-share model, gave spectrum an explicit value, and carved out an independent regulator in TRAI.

For the first time, the industry had a viable business model. A consultant who has watched the sector for 25 years told me NTP 1999 is still the best policy document, even if you compare it to those that came after it, because it first set out to explain what it wanted to do, and then changed the paradigm.

As for Airtel, it not only survived the regulatory body, but kept emerging as the biggest player as it contended with every change.

The second body: capital and technology

Surviving those challenges means continually building, and building serious networks takes cold, hard, up-front cash, the kind that Airtel, as a first-generation company with no oil business to lean on, simply didn’t have. Airtel had to learn to grow on money that wasn’t in its hand. That’s the second body.

One of the pivotal moments in the company’s history was a lunch between Mittal and Ericsson president Kurt Hellström.

“I have one request,” Mittal said. “I don’t have the money to pay you.”

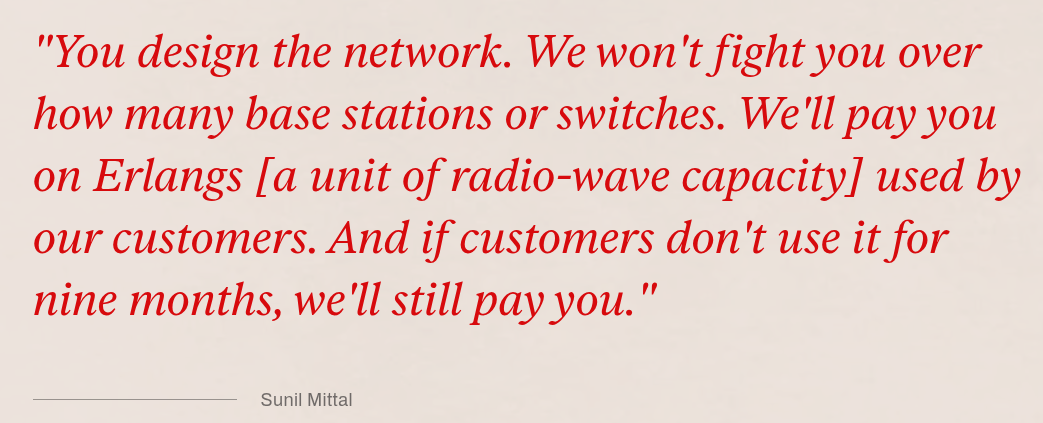

Hellström asked if Airtel could pay 15% upfront, and when the remaining 85% could be settled. Mittal said, “I will pay you in happiness. Happiness is when people are making calls on the street and they are happy.”

This lunch — which Mittal notably even didn’t have enough money to pay for — was meant to be a pitch for a $27 million equipment order, but it turned into a revenue-share deal between Airtel and Ericsson. And this was done well before anything was even built.

I think of this whole era as a bid-first, build-later philosophy. Key to this philosophy was Akhil Gupta, the long-time vice-chairman of Bharti Enterprises. In his view, perfection can always be achieved as you move ahead, but an advantage lost because of slow implementation can never be recouped. Airtel opted for speed over perfection, and speed won.

As part of this philosophy, Gupta cracked the idea of outsourcing everything that wasn’t core. It was a concept so unheard of that colleagues reacted as if he was suggesting they sell the family jewels. It’s why they made a decision no telecom CEO had ever made before: outsource their whole network to third-party vendors. In this case, that was Ericsson.

In his book, “Some Sizes Fit All”, Gupta outlines the details of the Ericsson deal in 2004. See, usually, a telecom equipment vendor wants to sell more boxes, while the telco operator needs to buy fewer to control costs. Gupta wanted to find a way to flip those incentives and ensure both of them were on the same page.

So, he deciphered the Erlang, a unit of radio-wave capacity, and offered to pay Ericsson per Erlang their customers actually used, while Ericsson would have control over how to design the network. That, as per Gupta, was the first time in telecom history where both the equipment vendor and the telco operator were on the same side of the table; both wanted more consumption.

Airtel transferred 1,100 engineers to Ericsson. They created a similar contract for IBM to handle its IT systems. Wildly, an Indian company was reverse-outsourcing its network to the West.

The next frontier to conquer was the tower network.

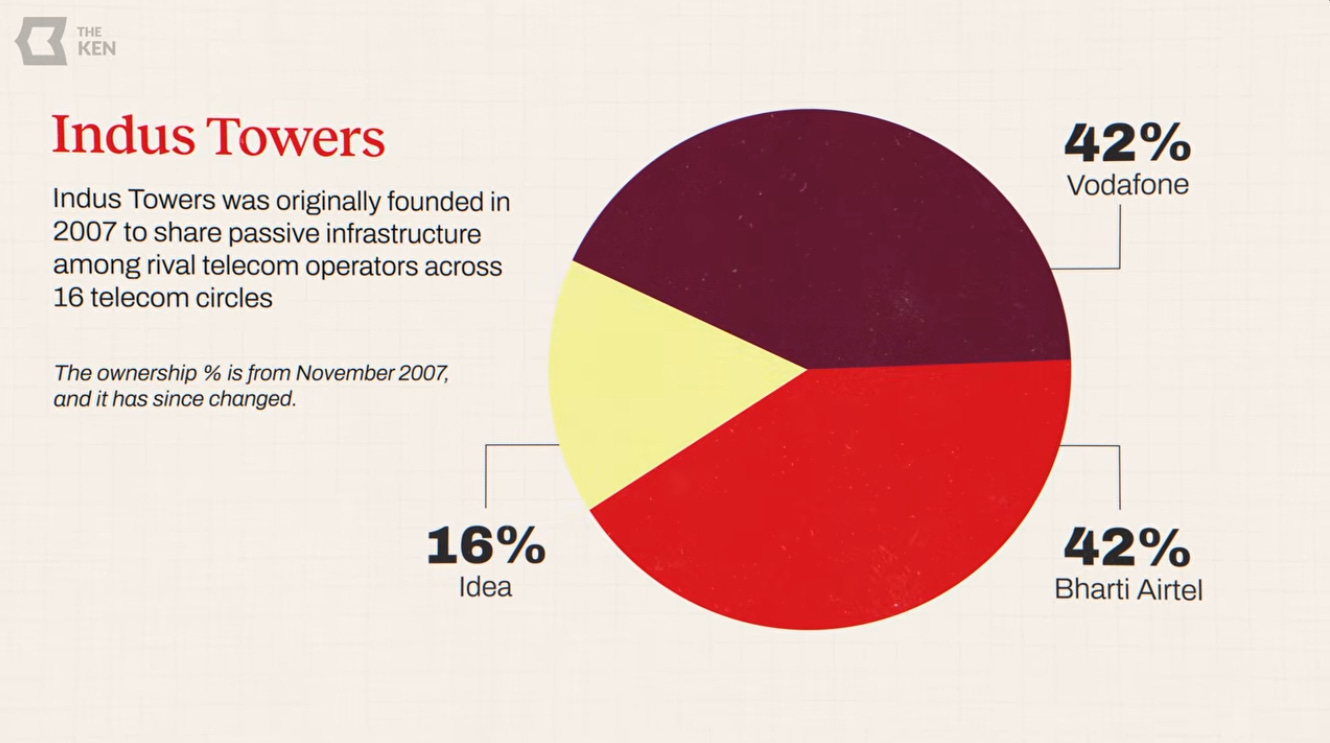

The cost of having exclusive towers is enormous, because the same asset can cater to four or five operators. It’s like the cost of travelling by chartered plane versus a commercial airline. So, in 2007, the bitterest rivals — Airtel, Vodafone, and Idea — pooled their towers into an entity called Indus Towers. In Gupta’s words, Indus was “a unique model in which a company makes more money when it charges its existing customers less, not more”.

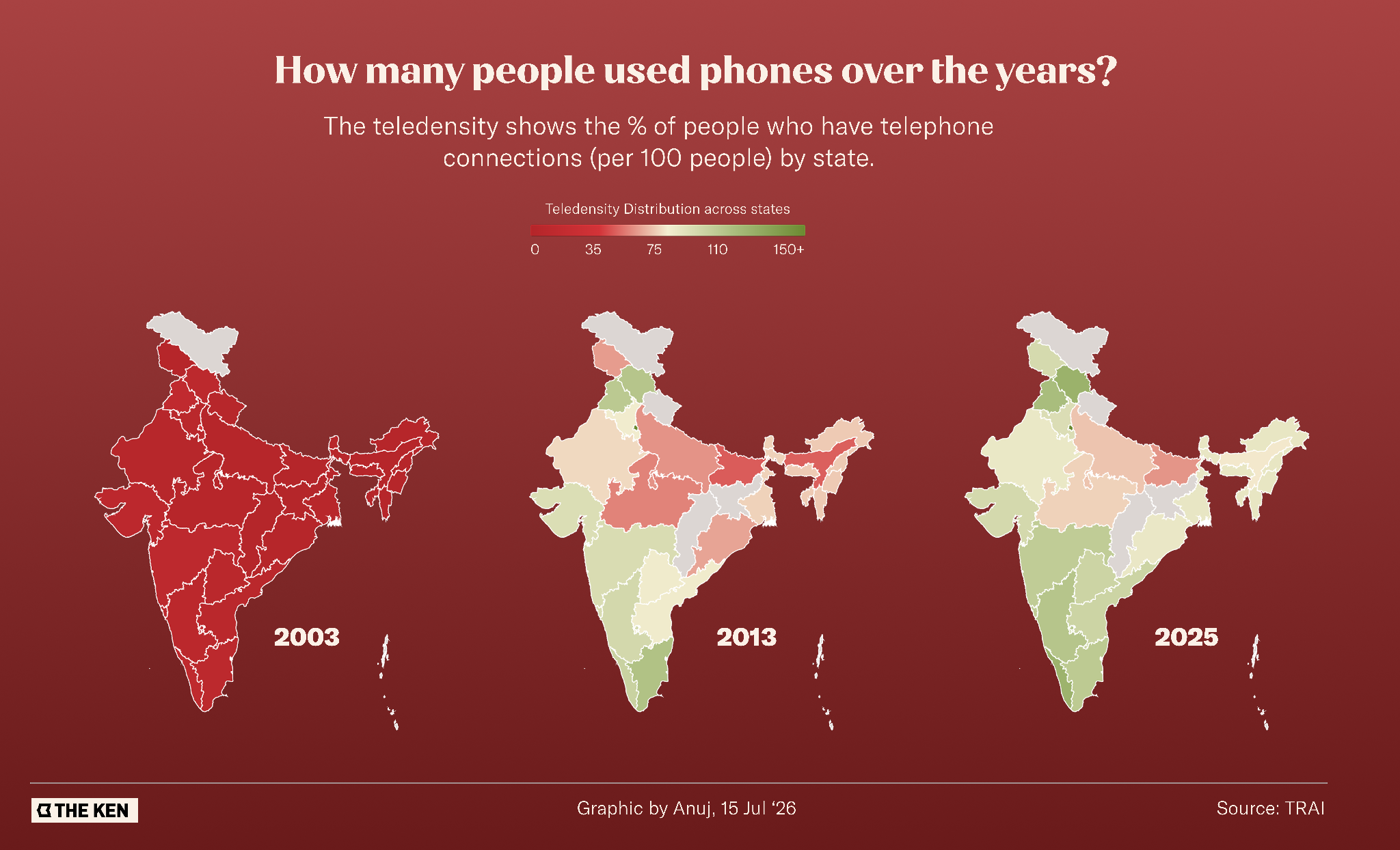

If the Airtel of the 1990s was Mittal learning to survive in a dog-eat-dog world, then the Airtel of the 2000s was him and Gupta learning to use scale and money so cleverly that they needed less to grow faster. The technology body moved relentlessly with 2G, 3G, 4G, and 5G, each roughly 10 times faster than the last, with spectrum you might gain one year and lose the next. Airtel thrived in all of this.

The third body: competition

In 2002, Airtel launched its IPO. That should have been a moment of celebration.

Instead, it was a life-and-death moment, because Reliance had the company in its crosshairs by offering free incoming calls and absurdly cheap outgoing calls. Importantly, it installed a fiber network that helped them legally bypass a “limited mobility” license that technically prevented users in one state from accessing the network of another. They’d essentially ensured national coverage now.

Airtel’s stock, meanwhile, fell from ₹45 to ₹20. Mittal wrote about it afterwards with a candour I’ve almost never seen from a CEO on the record: “I felt that if we stood up at this time, the storm would just blow us away[…] Lie low, I said, and we will live to fight another day.”

He also told his colleagues, “Everyone expects us to lose, but if we don’t, we will make history.”

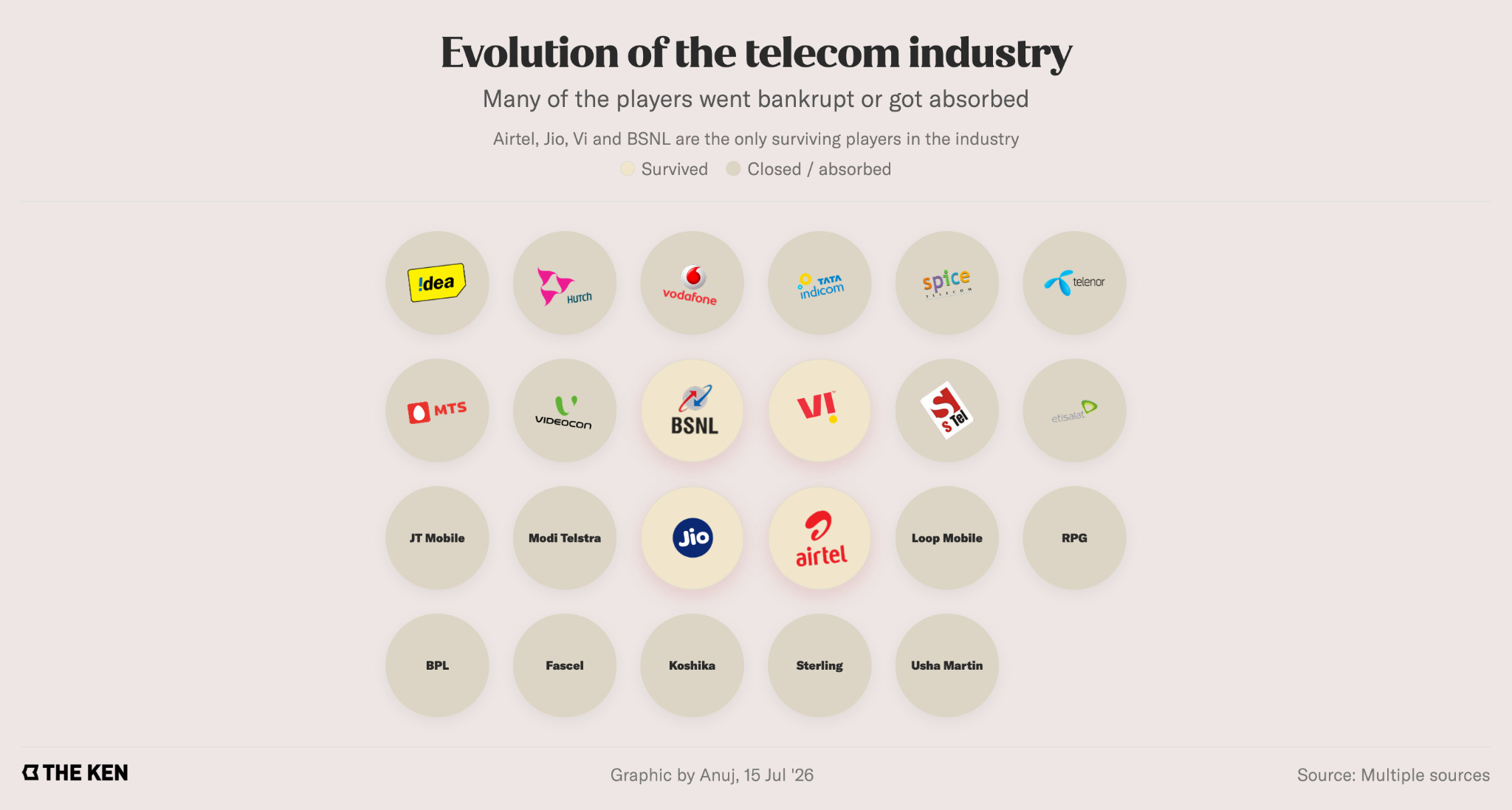

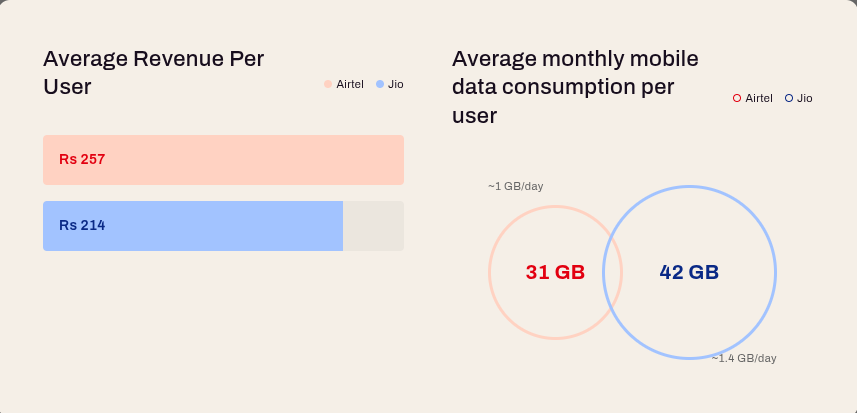

As it turned out, they did. Airtel walked in as a high-margin, low-volume company, then walked out understanding that India was a high-volume, low-margin market. Scale is the ultimate advantage in telecom.

15 years later, Reliance came back as Jio, with everything being free. Voice was free forever; it was just data on an all-4G network. Meanwhile, 65–75% of every incumbent’s revenue was voice. One person I spoke to put it bluntly: he didn’t give Airtel more than a 30% chance of surviving.

But Airtel prepared for Jio like it was war. They wouldn’t let a single premium customer go. The focus of Gopal Vittal, now the CEO of Airtel, was maniacal. If you slipped a new SIM into your phone, Airtel would obsessively figure out why and would offer you a deal to come back.

And then, Airtel made a move that went against the grain of scale in telecom: it shed its own customers.

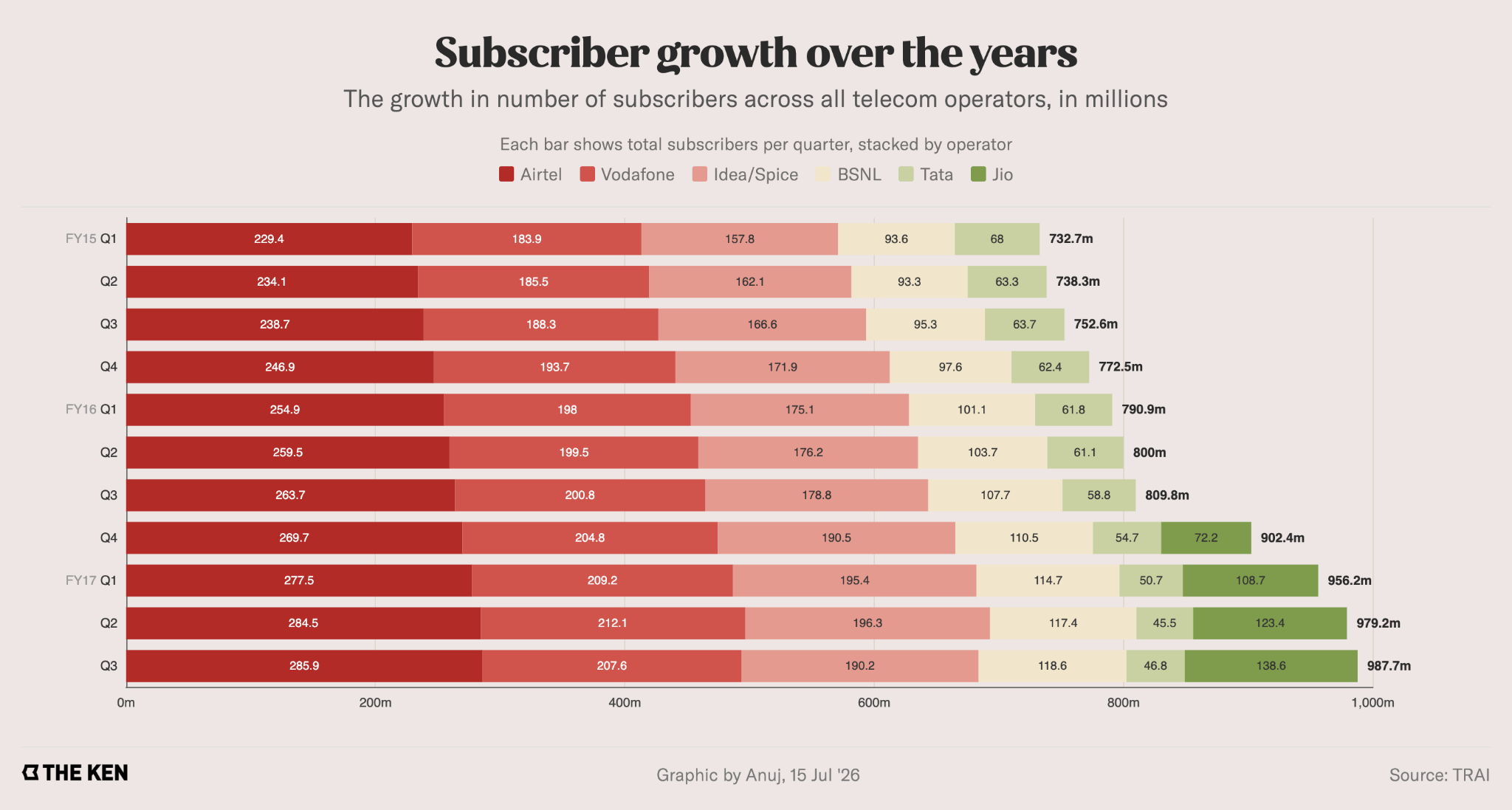

Airtel went from having 333 million subscribers to 284 million, shedding 49 million, by simply re-defining who a subscriber was based on a minimum ARPU plan. They were willing to lose what was equivalent to a small country’s population, because those low-value users clogged the 2G network that could be re-farmed for 4G.

There’s a beautiful irony in this: Airtel started as a premium player, was forced by Reliance to go mass, and then went back to premium when Jio emerged, but this time of its own choosing. As someone told me, when the sector started collapsing, it was like taking candy from a kid, and Airtel did it best.

Everyone thought Airtel would roll over like Vodafone. But if Jio were honest, they’d admit Airtel shattered their dream.

Mittal spent his whole career selling visions to partners far larger than himself and getting them to bet on him even if Airtel’s presence was tiny. Now, he’s free to make bets with a multi-decade horizon, even riding the AI and hyperscaler wave. Mittal has consistently been irreplaceable, but he’s now building a plan to make himself irrelevant to the future of Airtel.

Can the RBI bring in the big bucks?

A few weeks ago, the RBI effectively gave local banks the green light to offer NRIs up to 7% interest when they deposited dollars. Those same deposits paid around 3-4% until then. For that rate to practically double, that too on a dollar-denominated asset, is an abrupt change.

When the banking system suddenly starts paying a steep premium to get its hands on foreign currency, it’s a sign something is wrong. That should come as no surprise. In the first half of 2026, India faced a severe shortage of dollars, while the Rupee kept getting hammered in forex markets.

The rupee crisis

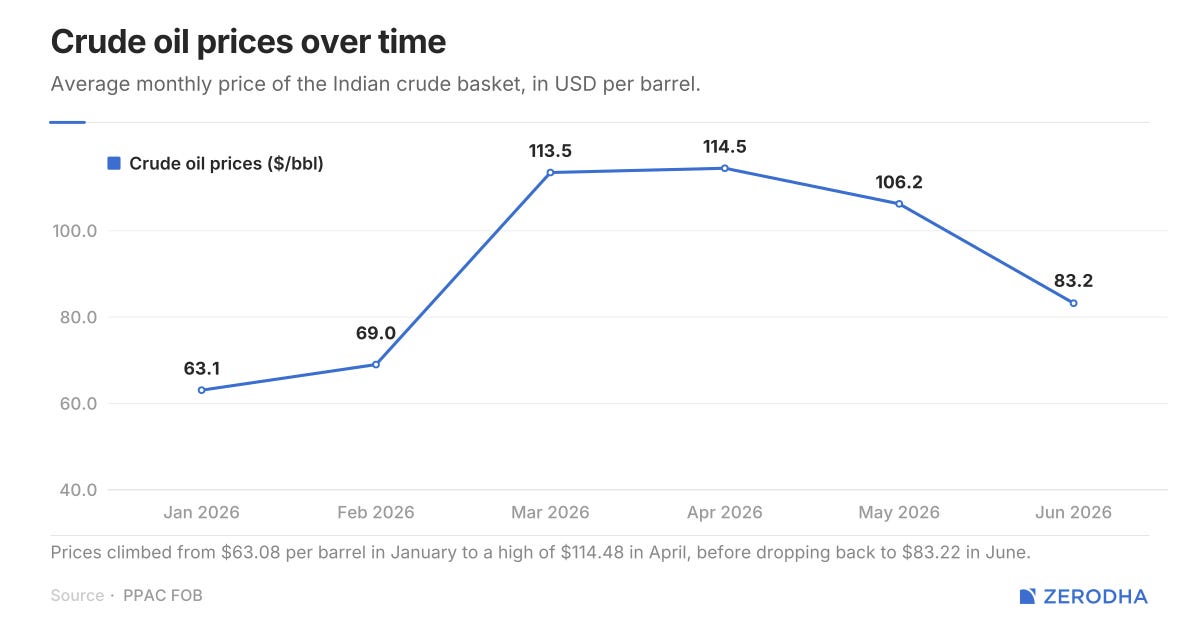

There were many reasons for this, some of which we ourselves aren’t sure about. But one facet of the problem, at least, was that India imports roughly 85% of its crude oil, and when war broke out in the Persian Gulf, the price of those imports skyrocketed. As recently as January, the average barrel of crude oil cost India somewhere between $62-64. With the war, that price shot up to nearly twice as much — to an average of $114 by April.

The consequences were terrible. In May alone, for instance, our oil and gas import bills surged by 75% year-on-year, to $17.5 billion — even though the number of barrels we imported barely changed.

Meanwhile, Foreign Portfolio Investors (FPIs) — overseas funds that invest in Indian securities — were fleeing Indian markets. The war didn’t start this outflow, by far, but the moment coincided with a trough in the foreign ownership of Indian equities, to a 14-year low of 14.7%.

Not every pipe was leaking. Net foreign direct investment — large, long-term stakes foreign entities take in India — actually improved to $6.6 billion in FY26, from an abysmal $1.6 billion the year before. Trade, too, had held up better than feared. Even while our imports were becoming more expensive, strong services exports and record remittances from Indians living overseas, made our current account look brighter. In fact, we posted a current account surplus in the March quarter. For all the fear and despair, our current account deficit for FY 2026 was just ~0.6% of GDP — an entirely manageable level.

In all, though, money was leaving the country. Through FY26, India saw a net outflow of about $30.8 billion in FY26 — more than six times the $5 billion outflow of FY25 — and that trend continued into the new financial year. It was a crisis. With demand for the rupee falling well short of supply, the rupee dropped to a record low of almost ₹97 against the dollar by mid-May.

The RBI intervened, selling over $60 billion of its foreign reserves since the war broke out, to prop up demand for the rupee. But it couldn’t burn through these emergency savings forever. The RBI needed to attract a massive, stable supply of new dollars.

There was one page in its playbook that it had used in a far worse crisis, back in 2013. That’s what it went for.

The FCNR bazooka

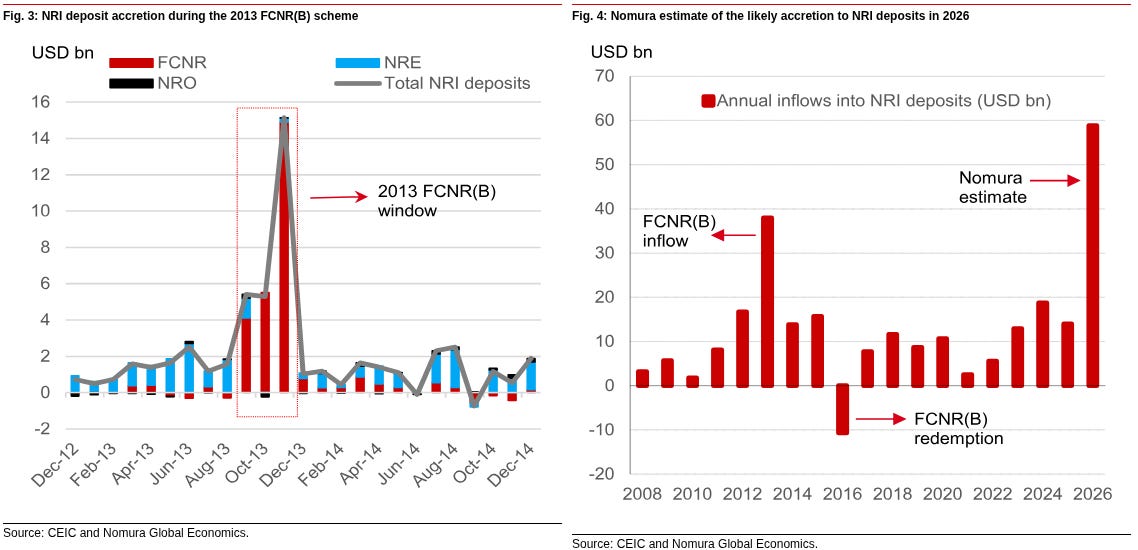

In 2013, the US Federal Reserve hinted that it might taper down its bond-buying program — which had been pumping easy money into the global economy ever since the Global Financial Crisis. This triggered a global panic called the “taper tantrum.” Investors aggressively pulled their money out of emerging markets. The rupee was crushed.

To survive that moment, the RBI turned to the Indian diaspora. They offered them a special window to deposit their dollars here, at home, through Foreign Currency Non-Resident (FCNR) deposits. It brought $26 billion into the country, stemming the tide.

The RBI is using that tool again.

The exchange rate problem

An FCNR deposit allows eligible NRIs to place their savings, like US dollars, directly into a fixed deposit with an Indian bank. The money stays denominated entirely in dollars. When the deposit matures, three to five years later, the bank returns the principal and the interest — all in dollars.

This can be a great deal for a depositor. They’re paid interest, of course. But more importantly, they take zero currency risk. Even if the rupee keeps falling through those years, their repayments are still calculated in dollars, leaving them unaffected.

This possibility has been around for a while. Historically, though, Indian banks would pay just 3-4% interest on them — barely beating inflation in the US. This was understandable — after all, those banks were taking a mountain of risk.

When an NRI deposits $100 with a bank in Mumbai, the bank doesn’t simply lock a physical hundred-dollar bill in a vault. That money feeds into its business. And since its business is in India, those dollars are sold in the open market in exchange for rupees — which are then loaned out.

There’s a problem, though. The bank now holds rupees, but eventually, it still has to pay the NRI back in dollars. If the rupee falls, that burden blows up.

Say, the exchange rate today is ₹90 to the dollar. The bank takes that $100, converts it, and gets ₹9,000 to lend out. Three years later, the deposit matures. If the rupee has weakened to ₹100, the bank suddenly needs ₹10,000 to repay the principle of $100. On top of interest, it also has to put aside an extra ₹1,000.

That’s a huge risk. So, on day one, the bank purchases a forward contract or a currency swap. Effectively, it locks an exchange rate for three years later, so that there are no surprises when it has to pay the NRI back. Only, this insurance is highly expensive — historically, costing banks roughly 3% to 3.5% every single year.

If the bank earns 8% on a rupee loan, and has to subtract 3.5% to pay for this hedge, there’s very little money left over to pay the NRI and cover the bank’s own costs. All it could offer NRIs, at the end of this all, was a dull 3-4%.

The RBI changes the math

On June 8, 2026, with a package of three regulatory changes, the RBI re-engineered that risk calculus.

First, the RBI removed the bank’s hedging burden by taking the currency risk onto its own balance sheet. Under this special window, banks sell the dollars to the RBI at the current spot exchange rate. When the deposit matures, the RBI will return the dollars at the same rate.

If a bank gives the RBI $100 today at an exchange rate of ₹90, it receives ₹9,000. But three years later, RBI will give back those $100 for the same ₹9,000 — even if the rupee has dropped! The bank simply bypasses the hedging cost. The swap only covers the principal, though, so banks must still manage the foreign currency required to pay the interest. Even so, it kills the risk the bank takes on the principal.

Second, the RBI exempted these fresh FCNR deposits from both the Cash Reserve Ratio (CRR) and the Statutory Liquidity Ratio (SLR). Ordinarily, banks must keep a portion of every deposit locked up as idle cash (CRR) or parked in safe, low-yield government securities (SLR). They couldn’t lend out 100% of its deposits. The effective return on that money was stunted. By waiving both requirements for this window, however, the RBI allowed banks to lend nearly every single dollar they raised as high-yielding commercial loans — boosting their earning potential.

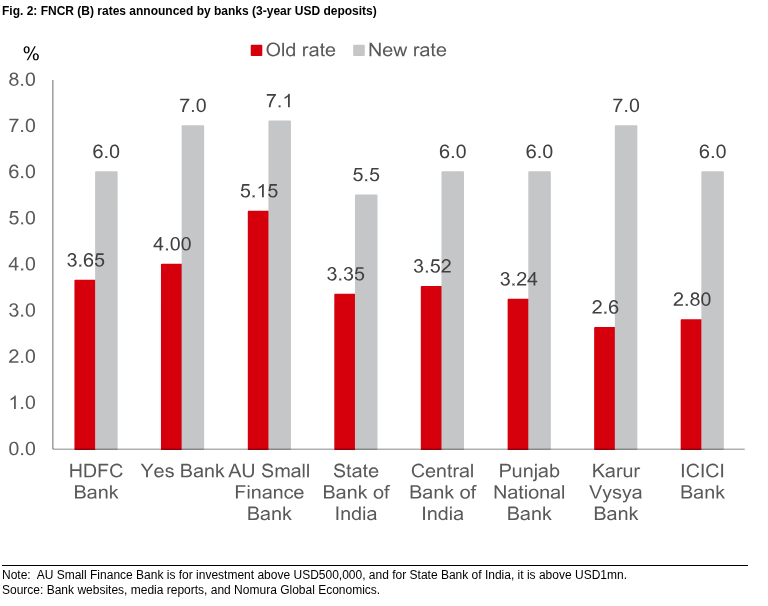

Third, the RBI removed the ceiling that capped the maximum interest rate banks were legally permitted to offer on FCNR accounts. The interest they could offer, now, could be decided by the free market. Each bank could determine its own rate, based on how urgently it needs funding and what yields it can generate — hence the wide 5.5% to 7.1% range visible today.

With these moves, the RBI effectively allowed banks to fish for high quality capital, without risk, all of which could generate returns.

The leverage story

But there’s another ingredient. While a 7% interest rate is great, that alone doesn’t bring in tens of billions of dollars. The real engine is leverage.

The RBI explicitly permitted Indian banks and their overseas branches to lend money directly to non-residents against these FCNR deposits. Since these loans are backed by the deposits itself — as collateral in their hands — lenders were happy to provide massive leverage.

Consider this: an NRI invests $1 million of their own savings. The overseas branch of an Indian bank steps in to lend that NRI an additional $9 million in dollars. The NRI places the combined $10 million into an FCNR deposit.

This is incredibly lucrative for investors. At a standard 6% rate, the full $10 million deposit would generate $600,000 in returns. Of that, let’s say the NRI pays 5.5% interest on the $9 million loan, or $495,000. That leaves $105,000 for the NRI. Their net return climbs up to 10.5% on their actual $1 million investment.

Meanwhile, India registers a fresh $10 million inflow, even though the NRI only brought in $1 million of original wealth. The remaining $9 million was generated from within the banking system. These would eventually have to be serviced and repaid, but for now, it stems the tide.

This is just one of the weapons the government has deployed. It also scrapped withholding and capital gains taxes for eligible foreign portfolio investors buying Indian government bonds, and opened a pipeline for foreign capital through GIFT CITY.

How much money is actually coming in?

According to recent updates, more than $9 billion has been mobilized under this special FCNR drive. That is substantial, but it remains below analyst forecasts of $30 billion to $55 billion.

The mechanics of the leveraged trade, to be fair, suggest that this would take time. For an NRI to borrow $9 million to deposit $10 million requires complex legal documentation, intense credit approvals, tax compliance reviews, and offshore funding lines. Such deals take weeks to assemble. And because the special window remains open until September 30, 2026, both banks and wealthy investors have a natural incentive to negotiate rates till then, and finalize their allocations closer to the deadline.

But does this make sense?

There’s one thing worth noting, though: the RBI has essentially assumed the risk for how the rupee moves over the next few years. This is practically a subsidy, meant to draw dollars in over the short term. It could suppress near-term currency volatility. But is it justified?

As Samir Arora from Helios argues, the subsidy basically pays for itself. If India can attract $40 billion to $50 billion through this scheme, that massive inflow will naturally strengthen the rupee. This will make it much easier for us to handle the national oil bill. To him, the money India we save on cheaper oil imports will outweigh whatever cost the RBI incurs by subsidizing the hedge.

But that’s not the only view. To former SEBI official Ananth Narayan, for instance, this can too easily descend into an economic game of whack-a-mole. The scheme props up the rupee today, but these dollars are not being earned organically by the Indian economy. They’ll go back out in three to five years.

In a best case, it buys us time — if we can plug the gaps in our economy over that period, it’ll make us more resilient when that outflow happens. If we can’t, however, this would ultimately have bought us little. We would simply have kicked a financial deadline down the road.

Tidbits

1. The Indian government has approved a massive ₹1.9 lakh crore investment scheme, including Mobile PLI 2.0 and Semicon 2.0. This initiative aims to boost local design capabilities and achieve self-reliance in semiconductor and mobile phone manufacturing.

Source: The Hindu BusinessLine

2. Smartphone brand OnePlus is reportedly ceasing its operations in the US and Europe due to financial challenges and a lack of market momentum. This move is part of a larger restructuring effort by its parent company, Oppo.

Source: Bloomberg

3. The Tata Group is planning to enter the shipbuilding industry with a massive ₹10,000 crore project in Kerala. This major investment is expected to significantly boost India’s maritime manufacturing and commercial vessel production capabilities.

Source: Business Standard

4. Tata Motors has asked the government to change the newly proposed Corporate Average Fuel Economy (CAFE) rules regarding carbon credits. The automaker argues that the current draft would actually make it cheaper for companies to pay penalties rather than invest in cleaner green technology.

Source: Business Standard

5. MakeMyTrip is reportedly preparing to file draft papers for an Indian initial public offering (IPO) using SEBI’s confidential pre-filing route. The issue is expected to exceed $1 billion.

Source: ET Now

- This edition of the newsletter was written by Rohin (CEO, The Ken) and Mridula.

Points & Figures by Zerodha

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how India’s retail lending landscape has transformed, using credit bureau data to reveal why lenders are moving away from unsecured loans and betting increasingly on collateral-backed credit.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

The Chatter by Zerodha

Our team at Markets spends a lot of time reading earnings call transcripts and listening to management interviews. Along the way, we come across plenty of interesting insights that are worth sharing.

That’s what The Chatter is for.

It’s a weekly newsletter where we dig through what India’s biggest companies are saying and bring you the most interesting insights into businesses, industries, and the wider economy.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops so that you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Very nicely explained!!

Good one