Hi folks, welcome to another episode of Who Said What? I’m your host, Krishna. For those of you who are new here, let me quickly set the context for what this show is about.

The idea is that we will pick the most interesting and juiciest comments from business leaders, fund managers, and the like, and contextualize things around them. Now, some of these names might not be familiar, but trust me, they’re influential people, and what they say matters a lot because of their experience and background.

So I’ll make sure to bring a mix—some names you’ll know, some you’ll discover—and hopefully, it’ll give you a wide and useful perspective.

With that out of the way, let me get started.

Why are AC companies struggling?

The hot summer that India usually experiences didn’t last too long this year. And that’s precisely what has made air-conditioning companies sweat.

In an interview with NDTV Profit, Vikas Gupta, the MD of PG Electroplast, explained what went down. By the way for context, PG Electroplast designs, manufactures, and assembles electronic components for other manufacturers.

“Because of the early onset of monsoon and high channel inventory, the overall summer selling season for air-conditioners got compressed. And it fell off beyond the anticipation of any of the industry players.”

Well, that’s a lot. Now let’s break down how this dynamic played out.

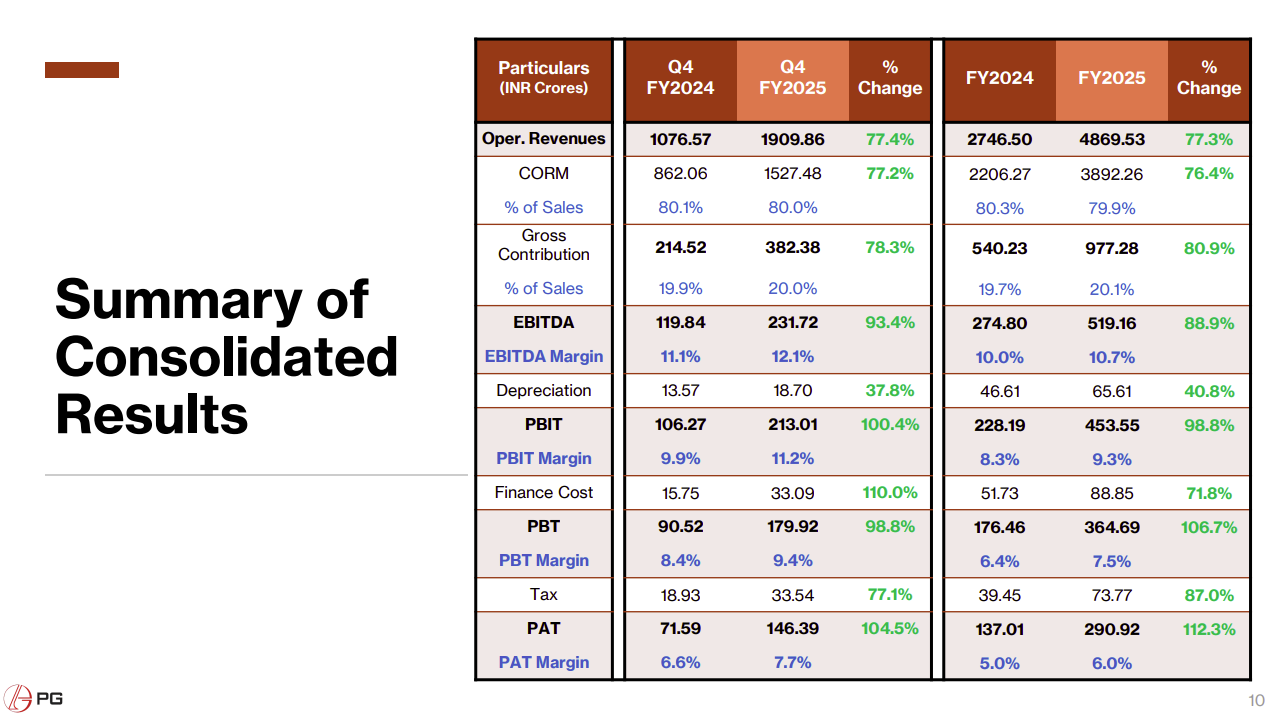

In the previous quarter (Q4 FY25), AC companies were swimming in soaring sales. PG Electroplast reported a whopping 77% increase in annual sales and around 100% increase in net profit.

In April alone, their AC sales jumped by 70%. They believed that the summer winds were blowing heavily in their favor, and they could sail through these winds at least until July.

So, to support that momentum, they expanded production massively by investing in more capacity. PG Electroplast had in their concall last year said that in FY26 their revenues will increase by a further 30%.

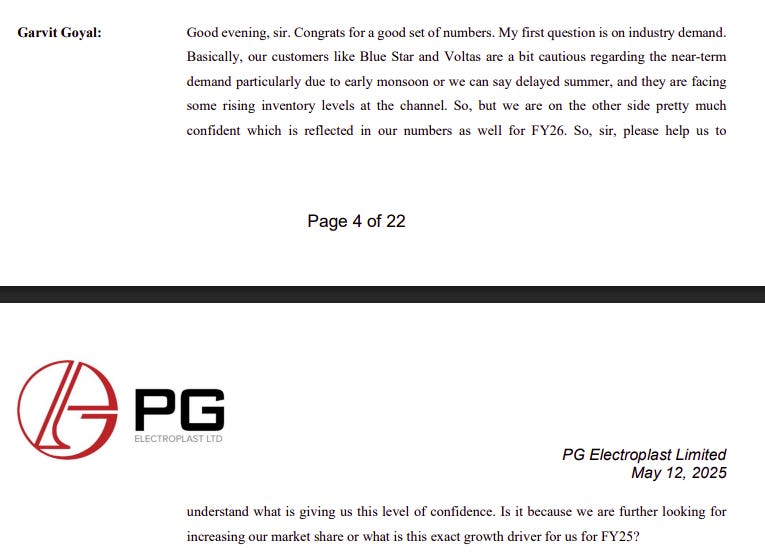

However, in the Q4 FY25 concall, one of the financial analyst raised a doubt around these future projections:

“Blue Star and Voltas are a bit cautious regarding the near-term demand particularly due to early monsoon, and they are facing some rising inventory levels at the channel. But we are on the other side pretty much confident which is reflected in our numbers as well for FY26. So, sir, please help us to understand what is giving us this level of confidence.”

This doubt has now come back to haunt PG Electroplast.

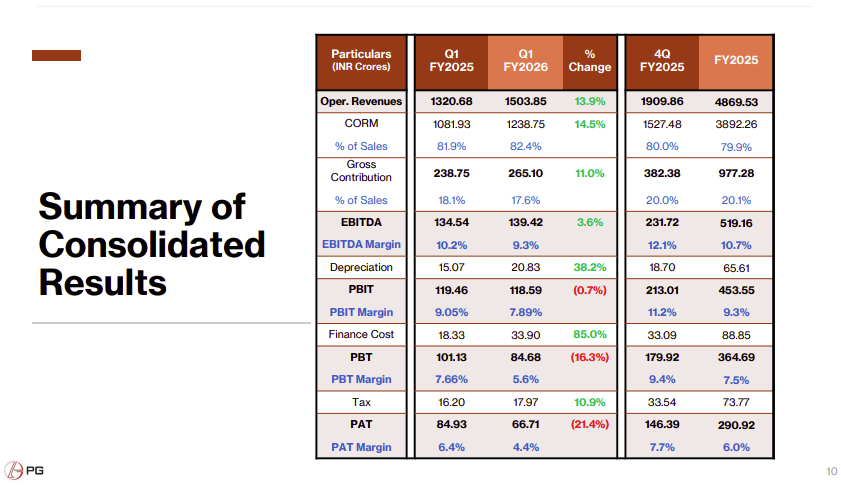

Fast-forward to the Q1 FY26 results. Compared to the same quarter last year, net profits got squeezed by 20%. Revenue increased by 14% — far lower than the 30% they expected.

The results were so disappointing that PG Electroplast had to lower their revenue projections for the whole year. They simply haven’t been able to sell enough ACs because the rains came far earlier than expected.

But that’s revenue. Why the profit shrunk so much can be traced back to their decision to stock up their AC inventory.

Now, remember that they spent on increasing their capacity — meaning money spent on more factories, hiring more people, higher rents. But these costs remain fixed — they cannot be reduced by producing less. So if sales fall, these costs will translate into big losses that can’t be offset elsewhere.

Their misery doesn’t end here, though. With higher capacity comes higher inventory. Due to falling sales, manufacturers were left with an excess of ACs that they could not offload anywhere else. This increased their inventory costs significantly.

Recovery from this looks difficult as most companies are lowering their projections for the year. They may expect some relief in sales due to the festive season, but the peak season for buying ACs only comes once a year. And this year, that peak never arrived.

What we can learn from this is that climate change is affecting the Indian economy in truly unexpected ways. It isn’t just resulting in hotter days, but also more unpredictability in the weather. This throws a wrench into the plans of even AC companies, that practically rely on hotter days for their sales.

Why is India's EV revolution stuck in a loop?

So, Partho Banerjee, senior executive of Maruti Suzuki, India’s largest car maker, in an interview with ET said this:

“It’s a chicken-and-egg situation. Till the time adequate public charging network is in place, customers are unlikely to use electric cars as a primary vehicle.”

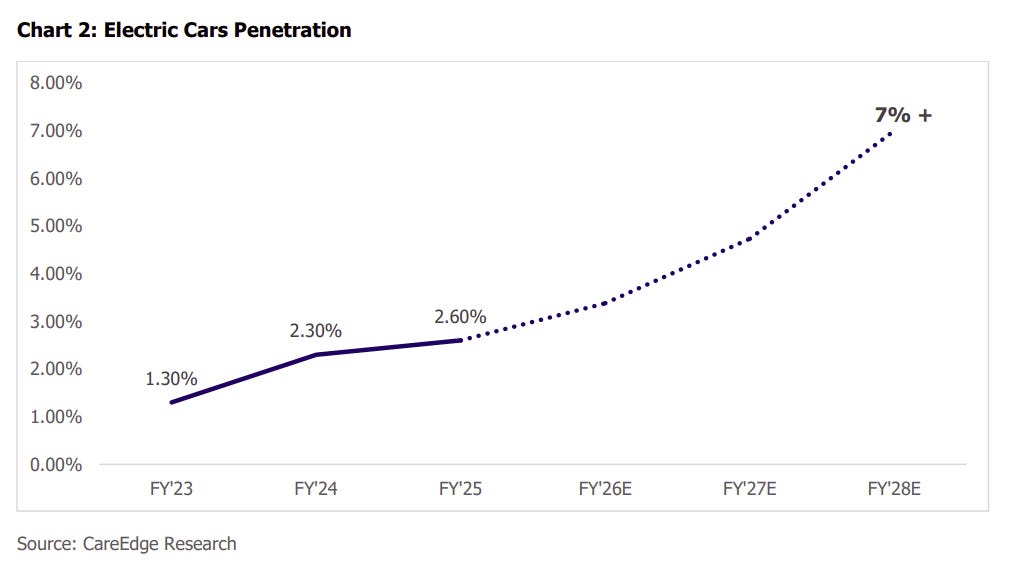

He highlights a very real problem. In 2024, 7.66% of all vehicles sold in India were electric. That’s scooters, rickshaws, buses — everything. The passenger car slice is far smaller, around 2.5%.

Banerjee says the problem is simple. Most people aren’t ready to make an EV their only car. They charge them at home, drive them for short errands, and keep a petrol or diesel car for anything longer. And unless there’s a visible, reliable public charging network, that base won’t get much bigger. Maruti’s trying to tackle it by planning to install chargers across the top 100 cities, but he’s blunt: without that network, EVs will stay the family’s ‘other’ car.

Meanwhile, Praveer Sinha runs Tata Power, the country’s biggest charging operator. Here’s what he told Moneycontrol:

“We have laid the groundwork for a robust EV charging infrastructure across the country, from Srinagar to Bengaluru… But the penetration of electric vehicles has not happened to the extent we were expecting. Many of our chargers are barely being used.”

Barely being used is polite. Public charger utilisation is in the low single digits. Which is why Tata Power has pressed pause on its plan to expand to 25,000 public chargers by FY28.

“Once EV penetration increases, you will see more and more of our chargers being utilised,” Sinha says.

And that’s the loop. Maruti says: more chargers, then more cars. Tata Power says: more cars, then more chargers. Meanwhile, the infrastructure that does exist is… well, not exactly what it looks like on paper.

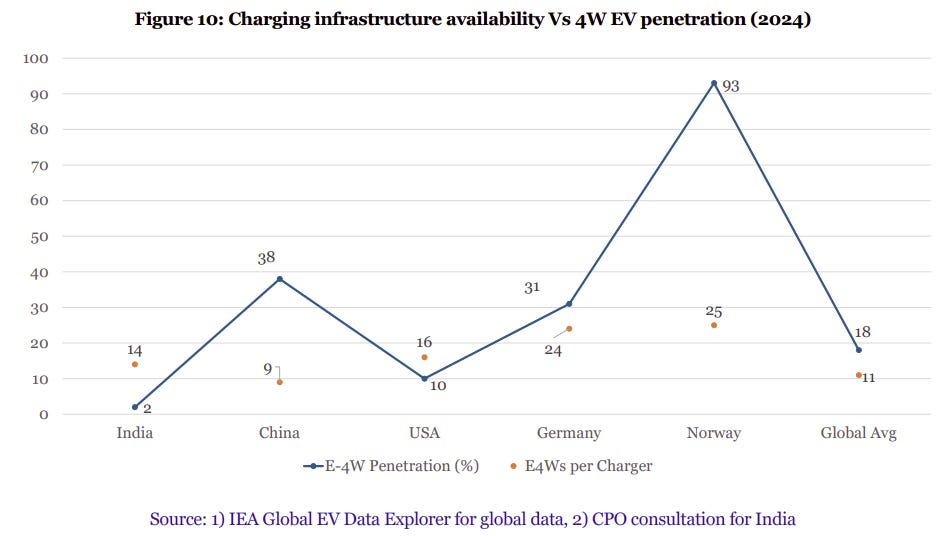

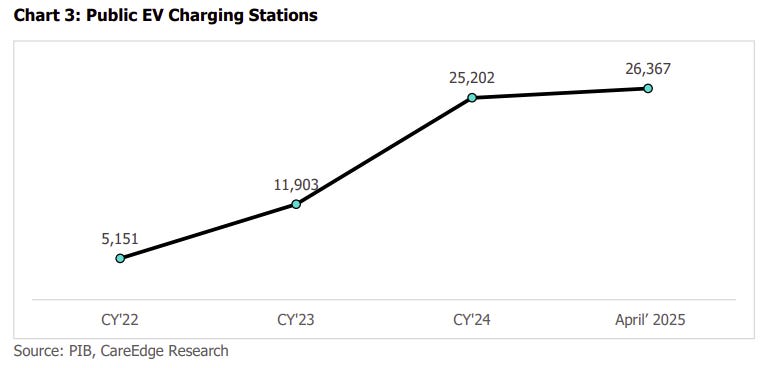

India officially has around 25,000 public chargers that’s about one for every 14 EVs.

That’s a better ratio than Norway, where it’s 25-to-1. But in Norway, 93% of new car sales are electric. The difference? Their chargers are where people actually need them, and they work. In India, too many are scattered as one-off units instead of clustered in hubs where they’d get real use.

Highways are the clearest example. The government has mapped 50 national highway corridors for fast-charging stations, aiming for one roughly every 25–50 kilometres. On paper, it’s a good plan. On the ground, coverage is uneven — some stretches have chargers bunched at one end, others have long gaps. And even where the chargers exist, they’re not always live 24×7: grid connections are weak in some spots, operators shut down overnight, or the sites rely on diesel gensets that aren’t there when you need them.

The PM E-Drive scheme has set aside ₹2,000 crore to fund 72,000 public chargers by FY26, with a cap of ₹10 lakh subsidy per unit. The idea is to put them along highways, at metro stations, toll plazas, airports, petrol pumps. But installing them is only half the battle. Charging operators face delays of months just to get grid connections from DISCOMs, have to cough up hefty security deposits, and often deal with outdated transformers that can’t handle the load.

And even when the charger’s up, price kills the appeal. Public charging costs more than double home charging in most cities.

India has all the pieces for an EV revolution — cars, chargers, government schemes, willing buyers. But they're not fitting together. It's seems like it is just about what already exists actually work.

Making sense of Trump's world, with Scott Bessent

Scott Bessent is a rare creature. He’s someone from a conventional Wall Street background. And yet, he has power in, and insight into, our new economic paradigm — where Trump has smashed a wrecking ball into everything we thought we knew about global trade.

We don’t know how he really feels about any of what’s happening, and we don’t know if he has any real power to change it. But that’s alright.

To us, at Markets, Bessent articulates the most coherent, intelligent-sounding expressions of what Trump is thinking. If there’s any logic to what’s happening, you’re probably going to hear that logic from Scott Bessent. If there isn’t, well, he’ll at least give you something to tear into.

That’s why we’re looking intently at a recent interview he gave to Nikkei Asia.

You may, for instance, wonder what Trump really has in mind, when he puts one of America’s highest country-specific tariffs on India. To Bessent, though, this might just be a negotiating tactic, and not a sign that we’re being singled out as a pariah state. As he says:

“He uses it [tariffs] for negotiations in foreign policy, just like now he said he wants India to stop buying Russian oil.”

That said, America’s primary adversary is still China. China, he says, “is the most unbalanced, or imbalanced, economy in the history of the modern world.”

To Bessent, it presents a unique threat to America. As he says, “Historically, our allies have been our economic rivals, and the Soviet Union was a military rival and a very small economy. China is new because it's the biggest economic rival and the biggest military rival. So it's difficult to deal with it.”

In fact, he paints China as fundamentally incompatible with the rest of the world’s economy. As he puts it “It's a non-market economy, and non-market economies have different goals.” What are they? To him, “much of what China does is they have employment goals. They have production goals, more than profitability goals.”

That’s what, he claims, America is trying to defeat.

But tariffs hardly seem like the signature of a market economy. What’s the broader idea around them? Does America really want a return to a protectionist world where every country hides behind its own borders?

Bessent, at least, does not think so. To him, this is all temporary. The way he tells it, Trump’s actually trying to remedy America’s inability to manufacture things like it once did. It’s a sort of shock therapy to shake things up, but it’s not a permanent fixture of American policy.

As he says it, “Over time, the tariffs should be a melting ice cube. If production comes back to the U.S., then we'll be importing less.” Sounds like a “production goal” and not a “profitability goal” to us, but we’ll let that slide.

That said, as any Indian born before the 90s will tell you, you don’t start manufacturing things just because you have import restrictions. So what’s the plan? Put simply, Bessent wants to change portfolio flows into investment.

See, historically, one of the reasons the American Dollar (and financial system, more broadly) has dominated the world is that everyone always thought of it as a fantastic place to buy financial assets. If you were looking to put your money to work, there were few other places this attractive.

Trump’s administration thinks they can, instead, get people to make long-term investments into America’s manufacturing sector: “Now, what we're trying to do is have more foreign direct investment and continue to make the U.S. the most attractive place, not only for portfolio capital, but for manufacturing relocation.”

Will that work? We don’t know. When you buy financial assets, it’s because you don’t want to closely manage how your money is used. With FDI, however, you have to roll up your sleeves and actually run a business in another country. It’s like the difference between sending someone flirty texts, and marrying them.

Can Trump give people enough confidence to actually make the switch? Who knows. We aren’t holding our breath.

If you’ve made it this far, please let me know if you have any feedback for me 🙂

🧑🏻💻Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

i love what u do guys

keep em coming

Tariffs that stick turn into a lose-lose game. Trump’s trying to script the rules for everyone else but global trade rarely follows one man’s playbook.

Interesting times indeed