A lending boom with fewer borrowers

And four other stories from RBI’s annual report

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Five ideas from the RBI's annual report

India’s tyre boom hits a pothole

Five ideas from the RBI's annual report

Towards the end of last month, the RBI came out with its annual report. It’s a 250-page monstrosity, filled with reams of data — income statements, schedules, payment-volume tables, footnotes on how gold is valued. Most people wouldn’t read something this dense. We wouldn’t either, if we weren’t trying to cover it for you.

If you can brave it, however, this dry report is filled with fascinating nuggets about India, its economy, and its financial system. Some of its headline numbers have made the news — such as the ₹2.86 lakh crore check the RBI handed over to the government. We won’t repeat those to you.

Here are five things you probably didn’t see in the headlines, however.

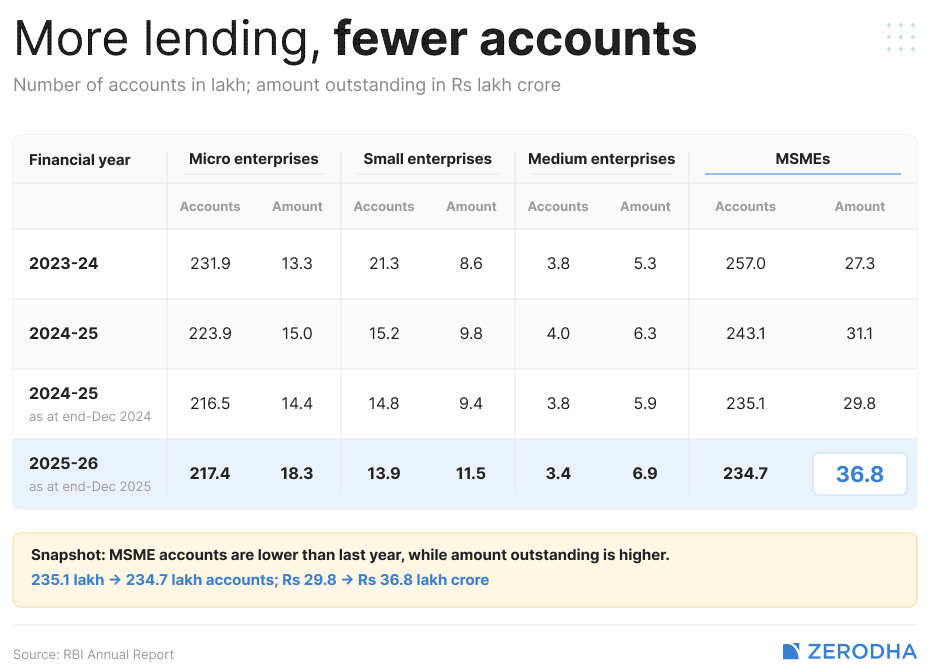

One: A credit boom without new borrowers

Between April and December last year, the amount banks lent to small businesses grew 23.5% year-on-year. The sector’s outstanding credit to micro, small and medium enterprises went up from ₹29.8 lakh crore to ₹36.8 lakh crore — a difference of ₹7 lakh crore in a single year.

By all accounts, this was a huge boom year. But there’s a twist: even though the money being lent grew immensely, it went to a smaller set of borrowers.

Over the years, the number of micro businesses receiving financing was roughly flat. The sector’s small and medium accounts, meanwhile, actually fell. At the very same time, however, the average borrower, across categories, had received more money.

Why would these two trends play out at once?

We have a few theories. For one, it’s just harder to lend to a new small business. Chances are, a new micro-borrower has no credit history, no audited accounts, and nothing to pledge. Giving them loans takes work — the effort of underwriting a ₹5 lakh loan to an unknown kirana shop is not very different from that in giving a ₹5 crore loan to an established company. The returns, meanwhile, are smaller.

India’s “priority sector lending” laws make banks direct a substantial amount of their lending to small firms. Their targets, however, are linked to the rupees they give out, and not how many borrowers they serve.

Together, these incentives push banks to reach for firms already on their books, handing them bigger checks, rather than finding new borrowers.

What could change this picture?

A major bottleneck many borrowers face is a lack of collateral. This is perhaps why the RBI, from April 2026, doubled the ceiling on collateral-free loans to small firms, from ₹10 lakh to ₹20 lakh. Ultimately, however, a firm with nothing to pledge is asking a bank to lend on trust.

Do banks actually have that appetite? That’s a question worth looking at next year.

Two: Money is getting more expensive for banks

Banks have an odd, convoluted relationship with money: they create money every time they give a loan, but are hemmed in by a series of statutory ratios. The specifics are too complex for what we’re doing here.

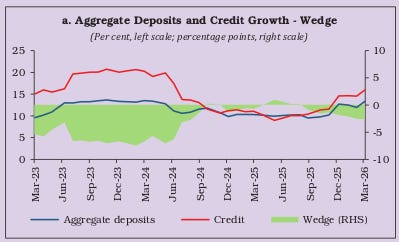

In a roundabout way, however, a bank’s fortunes are tied to the rate at which they can procure money. That has been tightening with time.

The cheapest source of money, for a bank, is the deposits people make with them. Over much of the last year, however, banks were increasing their lending faster than they could grow their deposits. In FY 2025-26, bank credit to the commercial sector went up by 15.9%. Just one year ago, that rate was much lower — 10.9%. Overall, bank credit grew by 17.1% through last year.

It isn’t that people aren’t making deposits. In fact, bank deposits, too, grew at a robust rate of 16.2% year-on-year. That’s reasonably quick, but it’s still almost a percentage point below the rate of credit expansion.

What does this gap actually mean?

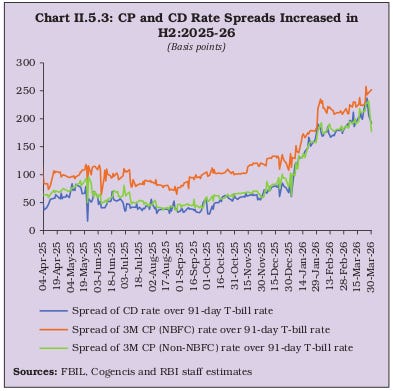

Banks won’t run out of money. All money, with the exception of hard cash, ultimately sits somewhere in the banking system. If a bank can’t grow the current and savings balances in its account, they can reach for something else. They could, for instance, try getting people to make fixed deposits with them. And if their lending outstrips that as well, they could go for wholesale funding — like certificates of deposit, which are short-term IOUs sold to mutual funds and insurers.

This is precisely what the report shows. In FY 2026, the banking sector’s total issuances of certificates of deposit were at ₹13.5 lakh crore — compared to ₹11.9 lakh crore one year ago. They were effectively scrambling to fund an unending surge in lending.

Different sources of money, however, come with different costs.

Wholesale money, for instance, is pricey, and reprices the instant rates move. In a crisis, it is the first to dry up, making it a path through which funding squeezes can curdle into failures. And over the year, the rates of this wholesale money grew as well.

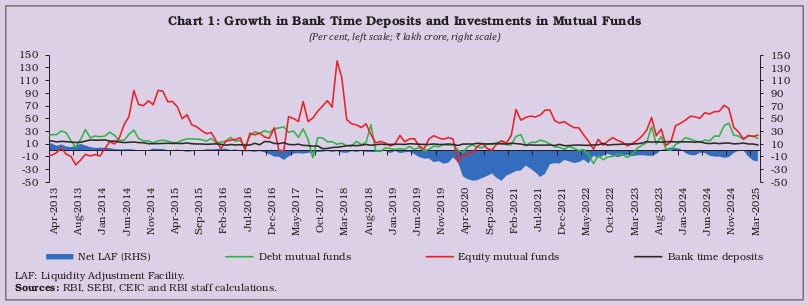

There’s a common story the newspapers tell you: that banks are starved for money because people keep putting money in mutual funds.

The report clarifies that there’s simply nothing to this. If anything, bank fixed deposits and debt mutual funds are complementary — they move together. Meanwhile, there’s no relationship between deposits and equity funds at all.

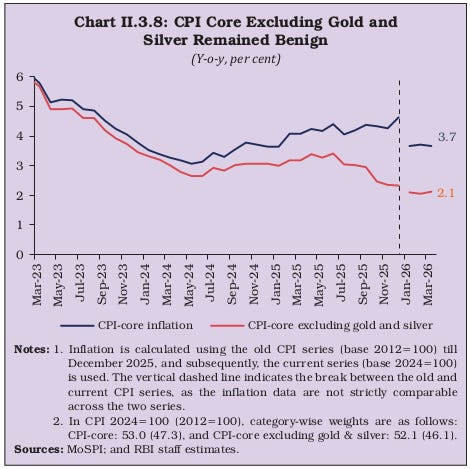

Three: What falling inflation means

Over FY 2026, retail inflation averaged 2.1%. It was well below the 4.6% we had seen a year ago, and nearly half of RBI’s 4% target. What does that tell us about RBI’s performance?

Well, try not reading much into it at all.

Judging the RBI by inflation rates is a tricky thing. Nearly half the consumer inflation basket is food, which barely budges when interest rates move. Food prices are a matter of the monsoon, of harvests, and of local logistics networks. The price of money has little to do with it.

Last year, food prices rose by just 0.8% between April to December. Just one year before, it had grown by 7.6% — almost ten times as much. October’s food deflation, in fact, was the steepest in the index’s history. It all sat on top of a costly base. Prices had jumped so much the year before that they seemed flat for much of last year.

Perhaps a smarter number to look at is core inflation: which ignores the prices of things like food and fuel, that the RBI has little control over. That figure came much higher, at 3.7%.

But this number, too, tells us little about the RBI’s performance. Half of it came from the prices of silver and gold, which recently saw a historic rally. Their prices were bid up by global investors buying safe havens because the world felt dangerous. Strip those out, and inflation dropped back to just 2.1%. If anything, that rate was dropping, especially after September’s GST cuts made many durables much cheaper.

Put all this together, and the inflation rate bore little connection to the RBI’s actions. This was simply a freak year. It saw geopolitical upheaval, choked global energy lifelines, jumpy commodity markets, and an unusually benign time for agriculture. None of this is information the RBI can use for policymaking.

Moreover, the RBI is changing its inflation basket, so the coming year will look different either way.

This year, it expects inflation to rubberband back to 4.6%, as base effects wash out and things regress to the mean. But if last year has taught us something, it is that the world is unpredictable. There’s nothing you can take for granted; least of all any normalcy in prices.

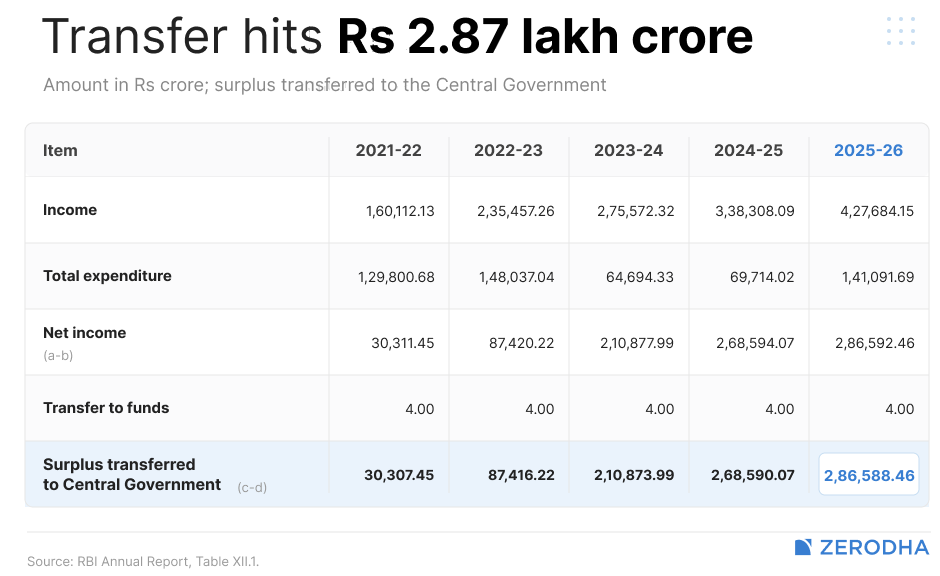

Four: The government’s big check

Since 2019, every year, the RBI has been handing over the government a big cheque, the size of which has become a small event. This year, it handed over its largest ever amount — ₹2.86 lakh crore — which people see as a windfall coming out of a good year.

This is often considered a “dividend”. In reality, it’s something different: legally, the RBI, once it covers its costs and sets aside its reserves, is supposed to hand any leftover money to the government.

How do you tell what’s “left over”, though? That’s an interesting story.

The RBI is supposed to set aside a buffer — a cushion of capital that would protect it against risks. A few years ago, after an ugly tug-of-war over the “correct” size of the RBI’s buffers, a committee set a band for how much the RBI could keep to itself. It would have to pay out the rest. That band, incidentally, was reworked last year.

That takes us back to the size of RBI’s check. Last year, the RBI’s income jumped by 26%. The size of its check to the government, on the other hand, increased by just 6.7%. The rest of its extra income — ₹1.09 lakh crore — was kept as part of its cushion. This was a massive increase from the ₹45,000 crore it kept aside the year before.

Why the change?

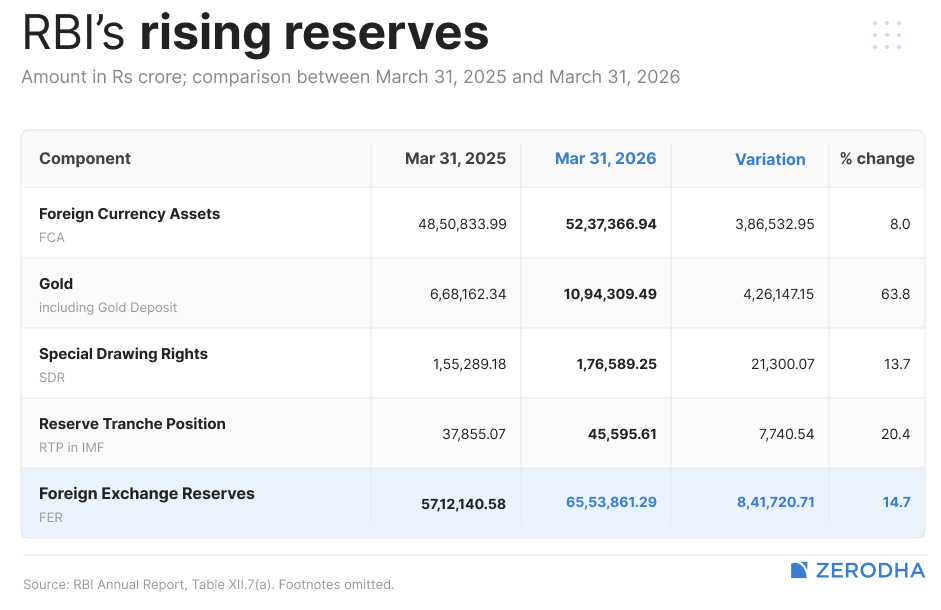

Much of the RBI’s “earnings”, this year, were paper profits. Its investments and reserves had swollen up through the year. Gold, in particular, ballooned. Although the RBI barely bought any — less than a tonne, in total — the value of its holdings leapt about 64%. This was amplified even further by the fall of the Rupee against the Dollar.

Those paper gains aren’t real, however, until that gold is actually sold. Before that, they can’t be paid to anyone. They’re simply part of what is called the “revaluation account”. This is meant to cushion against a swollen balance sheet. It would be counterproductive to hand that over to the government as surplus profit.

Five: What the RBI is building now that UPI is finished

India’s payments ecosystem has one world-renowned success — the UPI. The system appears unstoppable. The UPI rails carried over 200 billion transactions last year, growing an incredible 30% year-on-year. About 86% of every retail payment in the country went through the system.

This isn’t where the RBI wants it to end, though.

So far, India has built out the financial rails to move money: shuttling between bank accounts in seconds. Next, however, its ambition is to make money programmable. For instance, you can program the rupee to create guardrails around where money can be spent.

The RBI has been experimenting with this sort of thing through its central bank digital currency. In Gujarat, Puducherry and Chandigarh, the RBI paid food subsidies in this programmable rupee, coded to be spendable only on eligible goods at ration shops. This eliminated the need to set up monitoring mechanisms to police leakage and corruption — there was simply nowhere else that money could be spent.

The next goal is tokenisation. It plans to issue financial assets as digital tokens, settled in the wholesale digital rupee. This would allow these assets to change hands at once, the way money currently flows through the UPI. The first of these to be brought on-rail were certificate of deposit — the funding tool banks leaned on so hard this year.

The other big project is around data: specifically, through the ‘Unified Lending Interface’. The ULI lets a lender pull together all sorts of scattered records — land records, GST filings, business registration, even a dairy cooperative’s receipts — making it much easier to take lending decisions. Over last year, the platform crossed 9.6 crore data requests, and signed up 117 lenders.

It’s worth tempering this enthusiasm with a reality check, though: there’s no guarantee that every such project will succeed. For instance, its retail digital currency in circulation actually shrank this year, from about ₹1,016 crore to ₹772 crore.

Even so, this is a fascinating glimpse into what money could look like just a few years into the future.

India’s tyre boom hits a pothole

We all treat tyres the exact same way. They aren’t an exciting upgrade, they are a classic grudge buy. Fuel got more expensive earlier this year. Now, your tyre vendor may be telling you that prices are going up again.

India’s four major listed tyre makers — CEAT, JK Tyre, Apollo Tyres, and Balkrishna Industries (BKT) — closed FY26 with factories running at high utilisation after a demand surge that followed last year’s GST cut on tyres. Then, in the last few weeks of Q4, the raw material picture turned sharply worse, raising the cost bill. The question that remains, then, is how they deal with these costs.

The scorecard

But before we get onto the story, let’s look at the headline numbers.

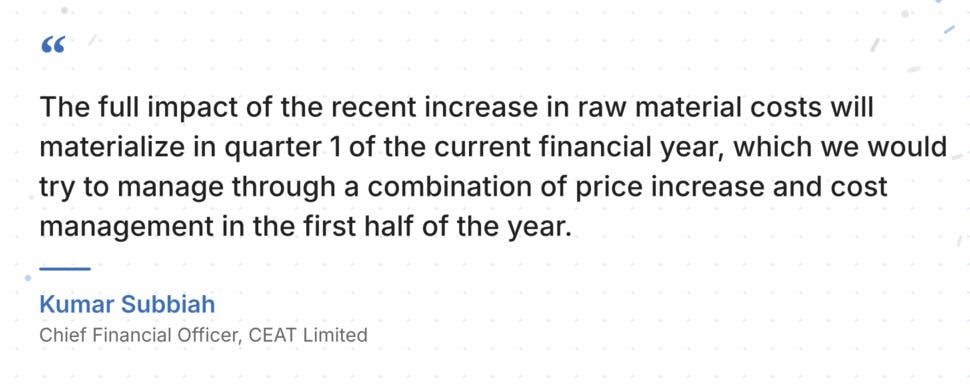

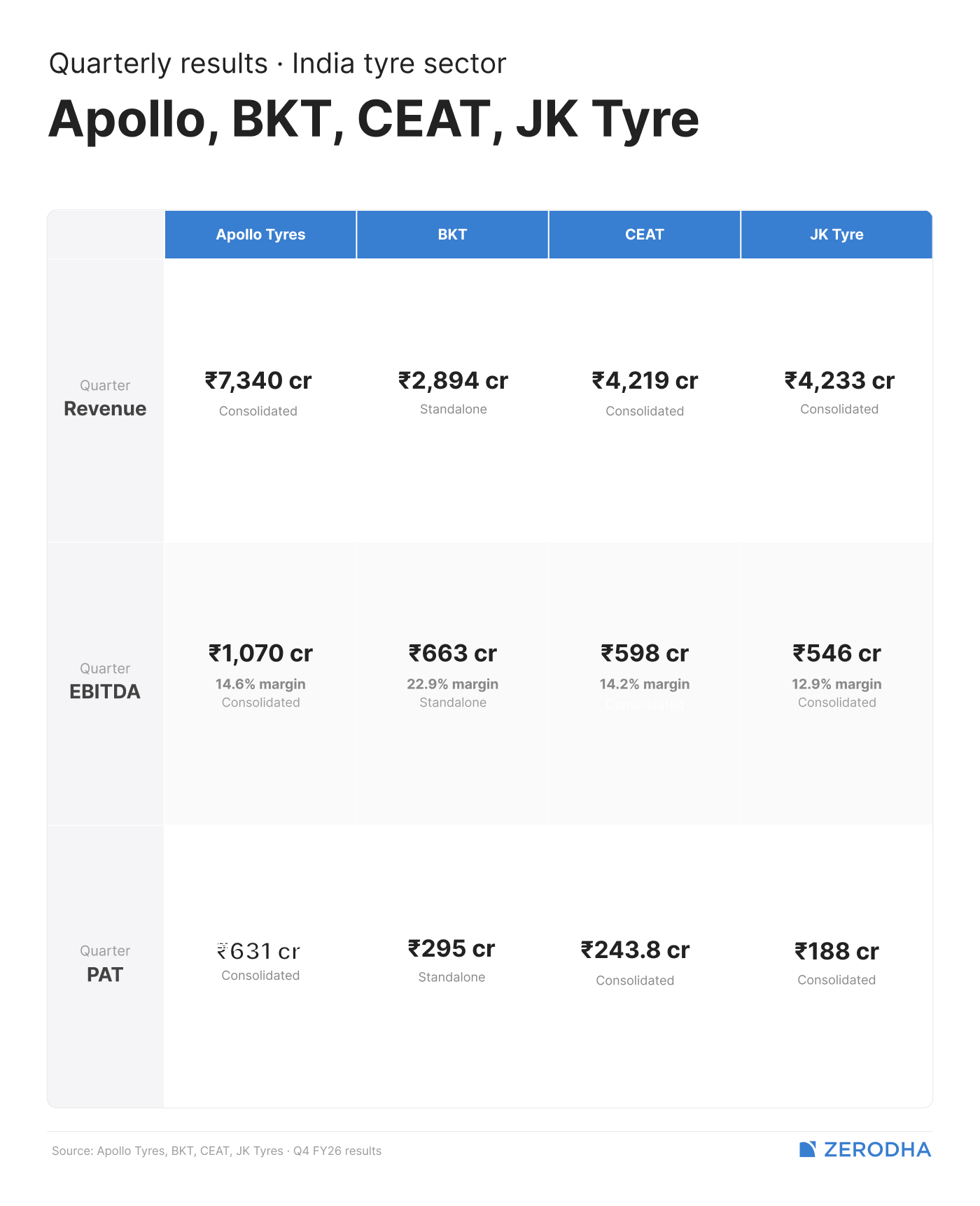

CEAT’s standalone revenue crossed ₹4,000 crore for the first time, finishing at ₹4,036 crore, up 18% year-on-year. The EBITDA margins stood at 14.5%. Standalone PAT was ₹283.6 crore, up nearly three times from a year ago. But CEAT admitted that they only held margins in Q4 because it was still running on cheaper inventory bought earlier. Their raw material costs are expected to rise 15–20% in Q1 FY27.

JK Tyre turned in its best annual performance on record. Their consolidated revenue for Q4 was up by 12% year-on-year to ₹4,233 crore, with EBITDA margins at 12.9% — 270 basis points wider than the same quarter last year. PAT was ₹188 crore, up from ₹102 crore in Q4 FY25. The company announced a ₹6,110 crore expansion plan to grow truck and car tyre capacity by 24% through FY29.

Apollo Tyres posted the biggest headline numbers, but with a footnote. Consolidated Q4 revenue was ₹7,336 crore at a 14.6% EBITDA margin. The reported PAT includes a one-time deferred-tax benefit of roughly ₹570 crore from a shift to India’s concessional tax regime. Strip that out, and the underlying business is more modest.

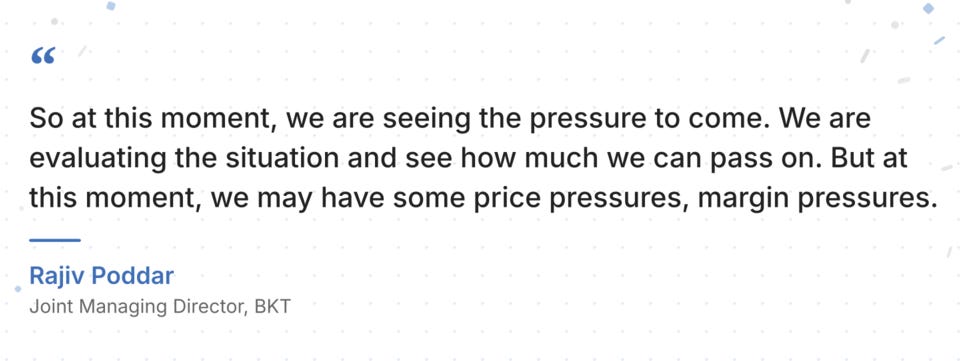

BKT had a quieter revenue quarter — standalone revenue was ₹2,894 crore, up just 2% year-on-year. But it also reported its highest-ever quarterly and annual off-highway tyre volumes in FY26. Its EBITDA margin of 22.9% ran significantly higher than peers. That’s because off-highway tyres carry more pricing power than truck or passenger tyres. BKT also admitted it faces near-term margin pressure.

The raw material reset

The West Asia conflict’s effects on crude and freight are covered in depth in our four-wheelers story this quarter. For tyre makers, the exposure to the same is unusually concentrated.

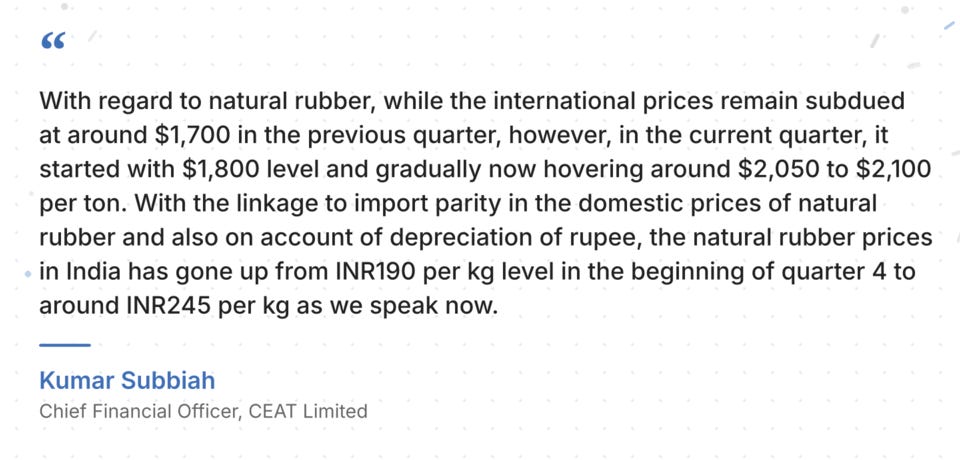

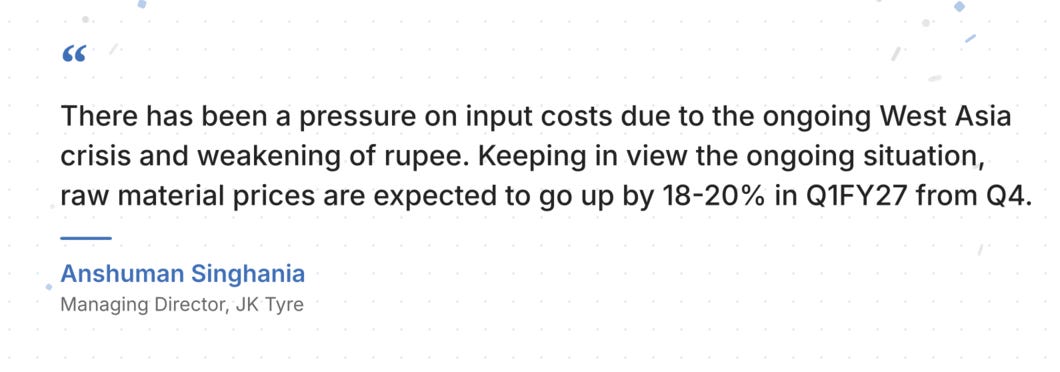

What’s specific to tyres is natural rubber. As we noted last quarter, India imports a significant share of its rubber, so tyre margins are exposed to global rubber prices and currency movements. That linkage meant the rupee’s move to ₹94 against the dollar during Q4 fed directly into domestic rubber prices. International natural rubber moved from about $1,800 per tonne to $2,050–2,100 by the end of the quarter.

The Q4 numbers were mainly insulated from the worst of this because companies generally tend to buy materials in advance. But everyone expects the bill to arrive.

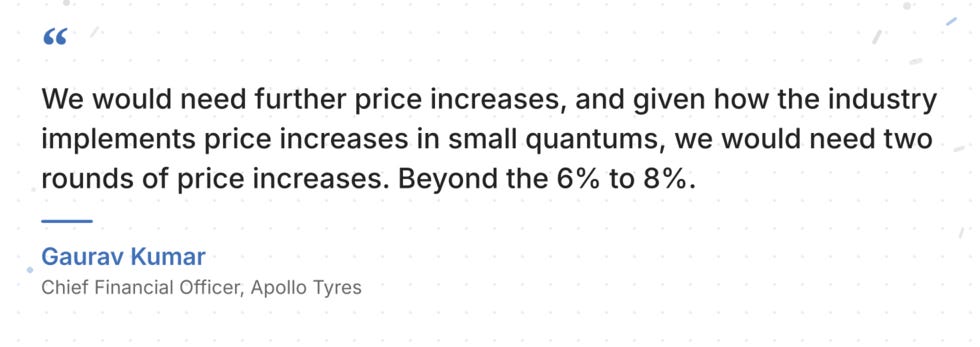

Apollo’s CFO, Gaurav Kumar confirmed the Q4 raw material basket rose only about 1% sequentially. The real reset lands in Q1 FY27, where they expect it to grow to the high-teens. Admittedly, Apollo’s already-announced 6–8% price hike is explicitly not enough to cover it.

CEAT expects those costs to rise to 20% of the bill by quarter-end, while JK Tyre guided to 18–20%. BKT, which had already absorbed a 4–5% rise in Q4, expected another 7–8% in the June quarter.

Can they raise prices without losing buyers?

To stave off some of the impact, every company has already announced price hikes to be borne by their customers.

CEAT, for instance, announced a 5% increase in the replacement tyre market between March and April, and is targeting another 5% through May and June. JK Tyre took a 4-5% price hike in tyre replacement and also flagged more hikes to come. Apollo announced 6–8% for Q1, and BKT took 3–5% across markets.

The problem isn’t that the companies can’t raise prices. It’s that different channels absorb hikes at different speeds.

See, OEM pricing, which is what tyre makers charge vehicle manufacturers, is contractual and adjusts with a roughly 3-month lag. For example, CEAT expected a meaningful OEM increase only from July 1, with only a small single-digit bump in Q1. So for about 3 months, tyre makers bear higher input costs before OEM prices catch up.

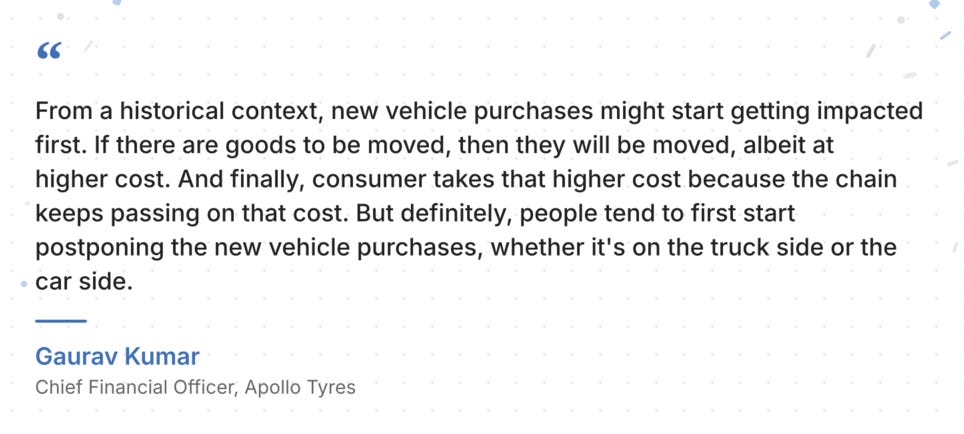

Apollo said the first hit from inflation usually shows up in new vehicle purchases, not freight movement. If goods have to move, trucks keep running and higher costs get passed along the chain.

In contrast, replacement demand is an easier channel to push cost increases through. That’s because the customers here will primarily be the end consumers of cars who don’t buy tyres on contractual terms, so there’s no lag. But it does not make it immune. Fleet operators, for instance, can still stretch tyre life, retread more, or delay non-urgent replacements when tyre prices rise sharply. CEAT said truck and bus replacement demand may slow, rather than collapse, if tyre price hikes become difficult for customers to absorb.

Betting big anyway

Still, a potential slowdown of replacement demand matters in an industry running near 90% utilisation and adding fresh capacity. If it slips even modestly, the new capacity may take much longer to pay off. And the scale of the capex wave that we covered last quarter has only grown stronger this time around.

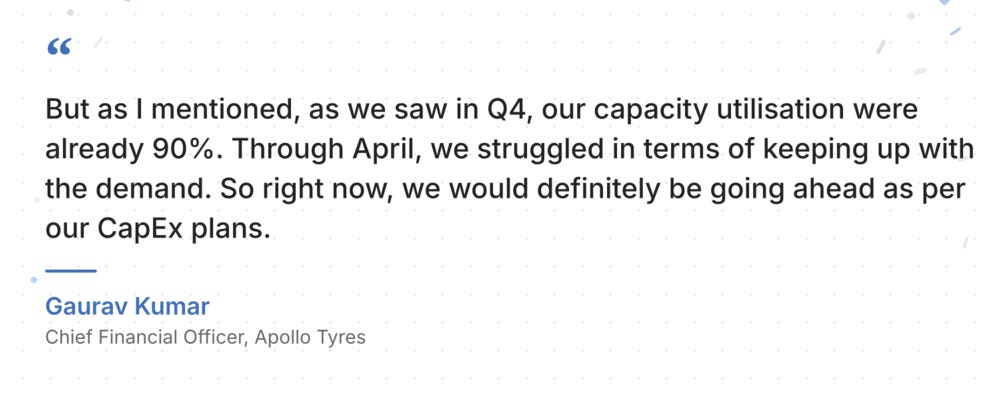

Everyone has fresh capacity to announce, and none of them have pulled back. Apollo has committed to ₹3,500 crore of FY27 capex, nearly 80% toward growth. Most of its FY27 capex is already committed. With utilisation near 90% and April demand still strong, the company sees little reason to pause its expansion plans.

At the same time, JK Tyre has added a fresh ₹4,980 crore to the ₹1,130 crore already announced, bringing its expansion program to ₹6,110 crore through FY29. BKT approved a fresh ₹2,000 crore tranche on top of the ₹2,800 crore it spent in FY26 alone.

The rural demand cushion is a meaningful part of this confidence. JK Tyre’s farm-sector volumes grew 58% year-on-year in Q4, with OEM farm volumes nearly doubling. Industry tractor sales in calendar 2025 crossed 10.9 lakh units, and Tractors and Farm Equipment (TAFE) company reported record sales in FY26.

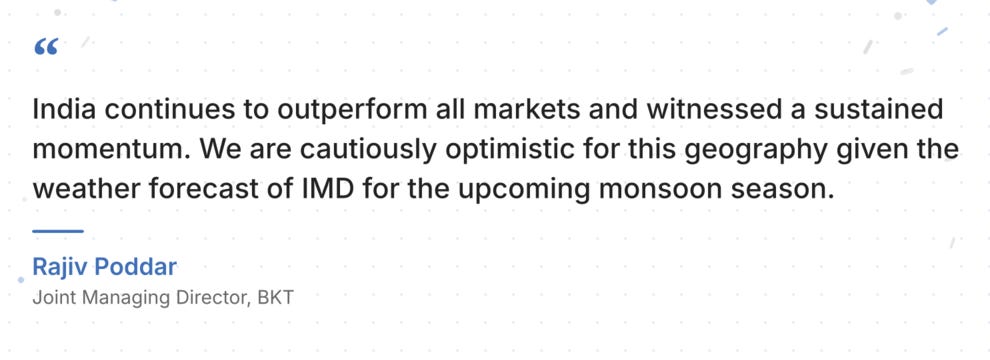

BKT’s core business is still off-highway tyres for farm, construction and mining equipment, and India has been one of its stronger markets. But that strength depends partly on rural cash flows. If rainfall disappoints across parts of Maharashtra and central India, farm equipment purchases could slow and tyre replacement decisions could get pushed out.

What to watch in FY27

The first real test will come in Q1 FY27. Q4 still had an inventory cushion. Tyre makers were selling into strong demand, but were not yet bearing the full cost of the raw material spike. By the June quarter, that changes. Natural rubber, crude-linked inputs and freight will flow more clearly into the cost base, while the first rounds of price hikes will test how much customers are willing to absorb.

That is why the next quarter matters more than the last one. If volumes hold despite higher prices, the sector’s margin recovery story remains intact. If replacement demand slows, even modestly, the recovery gets pushed out. The companies may still grow, but they will be growing into a tougher margin environment.

FY26 ended with India’s tyre makers running their factories harder than they had in years. FY27 begins with the same factories and commitments, but with a cost base that has shifted meaningfully against them. The companies aren’t wrong to be confident about the long run. But the next two quarters will tell us how correctly the confidence has been calibrated.

Tidbits

Green SM Enters India’s EV Cab Market

Vietnam’s Green SM (Vingroup) launched electric taxi service Green SM Limo in Delhi-NCR, planning a 10,000-vehicle fleet, a year after BluSmart’s collapse raised viability questions about all-electric ride-hailing in India.

Source: BSHeat Stress Costs Indian Farmers 54 Workdays Annually

Indian agricultural workers lost 163.3 million work hours to heat stress in 2024 — 54 days per worker, up 52% since 1990 — threatening food production and inflation, per an ECIU study.

Source: Financial ExpressHeatwaves Dent India’s Apparel Export Output

An NYU Stern study found Indian garment factories supplying Uniqlo, Tesco, and M&S face up to 10% productivity losses from extreme heat, threatening the $39 billion apparel export industry employing 45 million workers.

Source: BS

- This edition of the newsletter was written by Pranav and Vignesh.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Ajay Srivastava on India’s place in the fracturing global trade order

The rules-based world trade order as we know it is fracturing, with weaponized tariffs and every country scrambling to secure its place in the new paradigm. We recently spoke to Ajay Srivastava, founder of the Global Trade Research Initiative and a former Indian Trade Service official, to make sense of how India is navigating this high-stakes shift. Our conversation dives deep into what Trump’s tariffs actually mean for global trade, why Bangladesh massively outperforms India in garment exports despite fewer resources, why India’s software giants haven’t made a serious bet on AI, and the broken links in India’s textile supply chain. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Thank you so much for the article 💯🙌🏼 helpful

Quite well written.